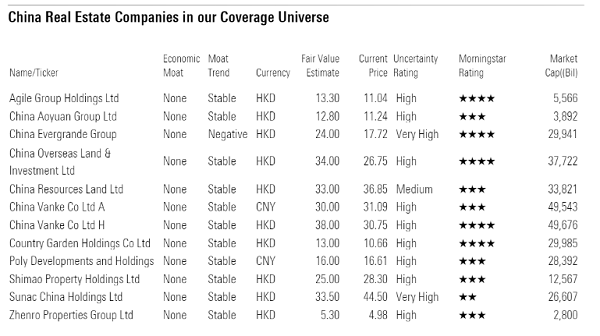

Many Chinese property developers reported lower January contract sales, as the property market was weighed down by the ongoing COVID-19 outbreak, which has restricted travel and business activities throughout China. While the exact timing for the resolution of the epidemic is uncertain, we expect the overall earnings impact on property developers under our coverage to be manageable. We should receive more information from the companies as they report their 2019 full year results later this month, but we expect limited change to our fair value estimates for the following reasons.

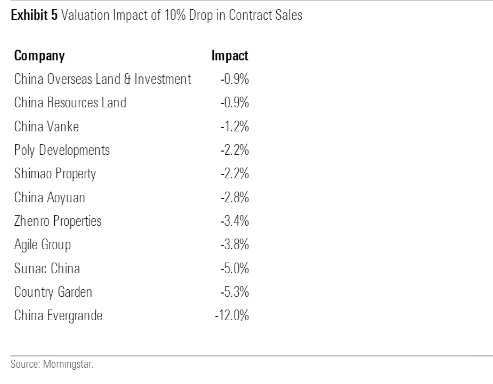

For one, first quarter activity tends to be a slow season for the Chinese property market, with most sales back weighted toward the second half of the year. Second, property sales, generally a large purchase for the household, are not subject to repeat transactions, or impulse buying. We expect the effect of the virus outbreak to be one of deferral of the purchase rather than the loss of the sale. Third, property sales in China consist mainly of presales. As such, we believe online sales to be a viable alternative. Furthermore, the government's accommodative monetary and administrative measures are likely to continue and could be expanded. Slower land acquisition and lower capital expenditure, along with easing financing conditions, will likely see developers through near-term liquidity issues. Lastly, assuming a 10% drop in contract sales, and subsequent pickup in late 2020, or 2021, the valuation impact to property developers appears to be minor.

COVID-19 hit to first quarter contract sales

Chinese property developers recorded sharply lower sales in January, compared with a year ago. For those under our coverage, contract sales were down 15% on average, ranging from less than 10% to more than 30%. Much of the decline was attributed to lower gross floor area, or GFA, sold as average selling prices held firm for most companies, logging a small low-single-digit gain on average. (Evergrande was the sole exception, which utilized extensive price incentives to boost sales). The sales decline was also partially attributed to the timing of the Lunar New Year, falling at the end of January this year, compared with early February a year ago.

Property sales are seasonal; Q1 is traditionally weaker

On the positive side, the first quarter of the year is generally a light period in terms of property sales. The residential property market in China tends to be weighted toward the second half of the year, with the first quarter contributing 15% and the first half contributing 40% over the past decade or so.

Mirroring the seasonality of property sales, property developers' land acquisitions tend to be back-end weighted as well. Over the past decade, land sales during the first quarter accounted for 20% of the full year total, while the first half accounted for 40%. Due to the spring festival, new starts during the quarter are generally limited to nearly 15% of the full year total. Hence, with slowing construction expenditures and lower land acquisitions, we do not expect slowing property sales thus far to pose significant liquidity challenges for the developers. For the sector as a whole, debt maturity is concentrated in the third quarter and beyond. For some more highly geared developers such as Evergrande and Sunac, the risk of liquidity challenges may rise if the COVID-19 outbreak constrains activity into the second half of the year.

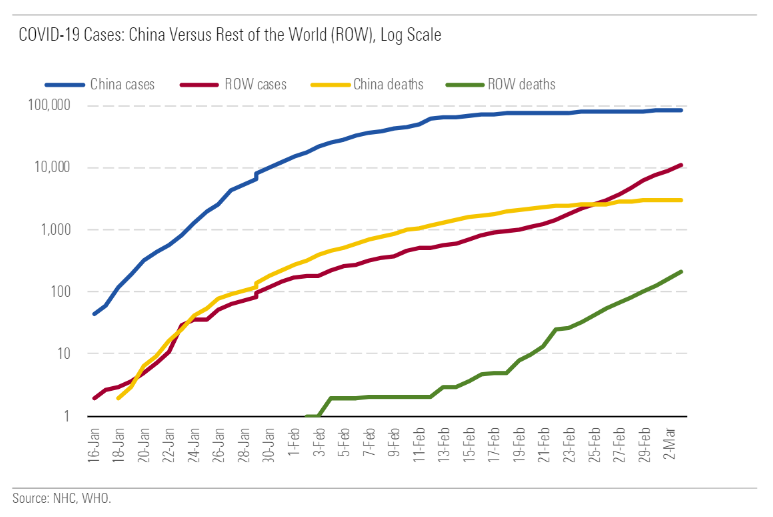

COVID-19 new cases are leveling off in China

Globally, while the number of COVID-19 cases continued to rise with new outbreaks, the number of cases in China is leveling off. New cases have continued to drop--the country recorded 125 cases on March 3, the lowest number on record. Starting from a week ago, efforts have begun to shift from controlling infections to restarting work.

For the domestically oriented real estate sector, we expect a quicker recovery relative to other sectors with more globalized exposure, given a self-contained supply chain and largely domestic customers. We expect the impact of the virus situation on the sector to be limited.

Easing monetary conditions and more favorable policies ahead

Reacting to the economic risks from the virus outbreak, the central bank has enacted numerous easing measures, utilizing almost all the tools at its disposal. The reverse repurchase agreement rates were cut in early February, and this was followed by lowering the medium-term lending facility rate by 10 basis points to 3.25% in mid-February. Subsequently, the one-year loan prime rate dropped to 4.05%, the first decline since October last year. The raft of measures enacted during the month is indicative of the PBOC's strong easing stance, a welcome change from its unwavering deleveraging effort over the past two years. Further, the property cycle has slowed during the past two years, now with 70-cities price growth decelerating to 6.3% in January, down from 6.6% in December. We believe this is a long-term sustainable rate. Coupled with the impact of the virus situation to be felt in the months ahead, the local governments and the central government are on the threshold of a policy shift, in our view. Already, some cities have begun adjusting policies to ease purchase eligibility on the demand side and expediting presales on the supply side.

Presales via online platforms

Property developers have greatly expanded their online presence, moving from the original marketing focus to implementing the full transaction cycle. Large developers are now further refining their online sales platforms, leading to integration with financing, registration, closing and after-sales servicing. It is important to note that most property sales in the primary market are presales, online sales may prove to be a viable alternative. While the actual impact is yet to be determined, the ongoing virus situation has led the developers to delivering property sales with greater efficiency through enhanced online capabilities.

Valuation impact not significant

With most Chinese property developers with landbank adequate for four to five years of development, our DCF-based valuation methodology generally accords more value to the back-end beyond the immediate projection period compared to a NAV-based valuation method. A one-off drop in contract sales or slower booking have limited impact on our fair value estimates. Given our expectation of the passing of the coronavirus situation and a quick rebound in sales during the second half the year, we expect our fair value estimates to be intact.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EWMG3XJM2RA4ZLC5J5M6SSVVZA.jpg)

.png)