Morningstar’s latest Global Investor Experience (GIE) Study found that Hong Kong and Singapore investors continue to experience a tax and regulatory environment that ranks ‘Average’.

Earlier this week, Morningstar published the second chapter of its sixth biennial GIE report, which grades the experiences of mutual fund investors on a five-point scale – ('Top', 'Above Average', 'Average', 'Below Average' and 'Bottom'). This chapter of the report, authored by Andy Pettit, Aron Szapiro, Grant Kennaway, Christina West, Wing Chan, Matias Möttölä, Germaine Share, and Natalia Wolfstetter covers 26 markets and has four independent chapters on Fees & Expenses, Regulation and Taxation, Disclosures, and Sales. The other chapters will be released later in 2020. You can find the second chapter here.

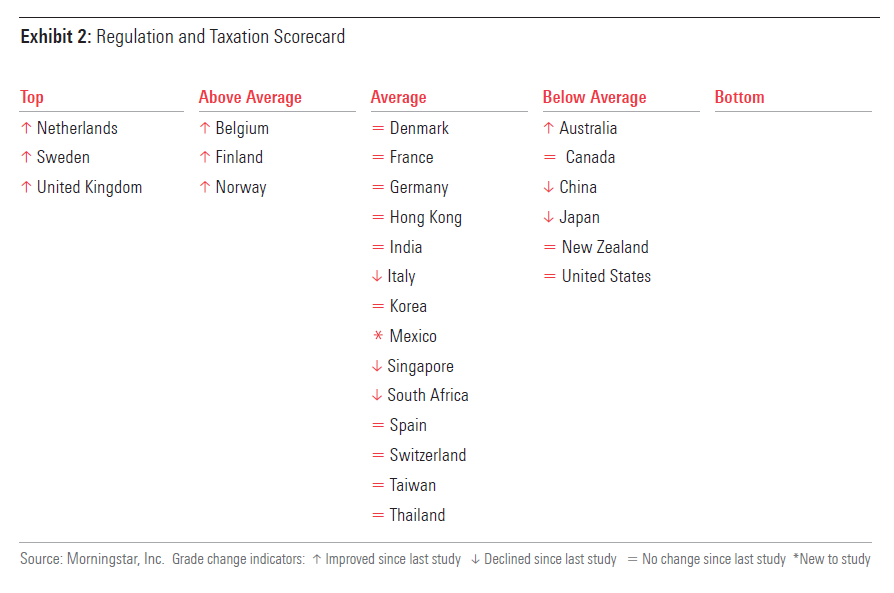

First, here’s a look at how all 26 markets scored:

Before we discuss key findings, let’s address the pandemic.

COVID-19

This chapter of the study was concluded prior to the COVID-19 pandemic. However, we’ve seen governments and regulators take a variety of different approaches to maintain market stability as well as assist businesses and protect investors during these times. Liquidity was already an issue high on many regulators’ agendas, and the volatile markets have put it back in the spotlight for many markets. We found that most impose limits on how much a product can invest in illiquid or unquoted securities and this reduces risks of forced sales and fund suspensions.

Global key findings

The report finds that regulation is not the sole driver of a market’s investment landscape, with aspects like competition and market-focusing events playing a big role. The authors note that markets vary in their policies to give people incentive to invest, but many markets have taken important steps to motivate large numbers of ordinary people to invest for their futures, from creating special tax wrappers to automatically enrolling workers in defined-contribution retirement systems. The most problematic tax policies are when arcane elements of the tax rules prompt investors to choose one product over another without a rationalized policy justification.

The Netherlands, Sweden, and the UK topped the table, in part because they provide strong incentives for ordinary people to invest, although the authors note that none has the best tax systems for ordinary investors. The four markets that performed poorly in previous iterations of this chapter—Australia, Canada, New Zealand, and the United States—continued to score poorly relative to other markets. “It may be that there was no focusing event or crisis to spur an overhaul of a legacy regulatory system that has worked well but has been eclipsed by other markets,” the authors explain.

Hong Kong

Hong Kong's tax policies are favourable to fund investors; capital gains and interest income are not taxed at all. However, fund distribution in Hong Kong remains dominated by intermediaries, with investors frequently paying the costs of distribution from fund assets. Overall, the Regulation and Taxation grade for Hong Kong is Average.

The investment industry is regulated by the Securities and Futures Commission of Hong Kong (SFC), whose main responsibilities include setting and enforcing market regulations; licensing and supervising intermediaries that conduct activities regulated by the SFC; supervising market operators and helping to enhance market infrastructure; authorising investment products and offering documents prior to their distribution to retail investors; overseeing the takeover and merger regulations of public companies and the Stock Exchange of Hong Kong's listing regulations; cooperating with regulatory authorities inside and outside of Hong Kong; and educating the investing public. Most of the regulatory sanctions are made public by the SFC.

The SFC has made several regulatory enhancements since our 2017 study to further improve a fund investor's experience. Since 2018, the SFC has required the disclosure of trailer fees and restricted the use of the word 'independent' by intermediaries that receive monetary or nonmonetary benefits from product issuers or have other legal or economic relationships with the product issuers. In July 2019, the SFC issued 'Guidelines on Online Distribution and Advisory Platforms,' which governs the online sales of funds and provision of online advice, including robo-advisers.

Investors in Hong Kong benefit from an investor-friendly tax regime that differentiates it from most markets in our study. Individual investors who earn income by trading securities are exempt from paying taxes on their capital gains, dividends, and interest income. Fund investors are also free from paying taxes on capital gains or interest on their fund investments.

While we continue to recognise Hong Kong's investor-friendly tax regime, we added importance to the regulation of fund operations and distribution because this is where we see a wide variation in practices that have important, real-world implications for ordinary investors. Disadvantages in this area compared with other markets in this study—such as the allowance of soft commissions, no separate disclosure of third-party research costs paid by the investor, and distribution costs paid out fund assets—have kept Hong Kong's Regulation and Taxation grade at Average.

Singapore

Singapore receives a Regulation and Taxation grade of Average. Regulation in Singapore features compulsory retirement savings with significant allowable contributions, and investors are generally exempt from all investment taxes. However, soft-dollar arrangements are common in Singapore, and investors typically pay for the cost of distribution out of fund assets.

Most funds registered in Singapore are unit trusts—the common term used for Singapore-domiciled open-end funds. That said, parliament announced a new structure for collective investments called Variable Capital Companies in October 2018. Under this structure, which is in the process of being rolled out, Singapore is encouraging fund managers to domicile their collective investments in Singapore as opposed to foreign markets such as Luxembourg or Ireland. Singapore also allows foreign-domiciled funds to register for sale in Singapore.

The Singapore Exchange Fidelity Fund protects customers in defalcation cases, potentially providing compensation up to SGD 50,000. Regulation enforcement is handled solely by the Monetary Authority of Singapore (MAS). All enforcement actions are public and listed on the MAS website.

While we continue to recognise Singapore's investor-friendly tax regime, we added importance to the regulation of fund operations and distribution because this is where we see a wide variation in practices that have important, real-world implications for ordinary investors. Disadvantages in this area compared with other markets in this study—such as the allowance of soft commissions, no separate disclosure of third-party research costs paid by the investor, and distribution costs paid out fund assets, have lowered Singapore's Regulation and Taxation grade to Average, which is one notch down from our previous study.

More details on both markets are available in the study.

Morningstar launched the Global Investor Experience study (GIE) in 2009 to encourage a dialogue about global best practices for mutual funds from the perspective of fund shareholders.

©2020 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

How are investors treated around the world?

Get the latest Global Investor Experience Study on regulation and taxation here

.png)