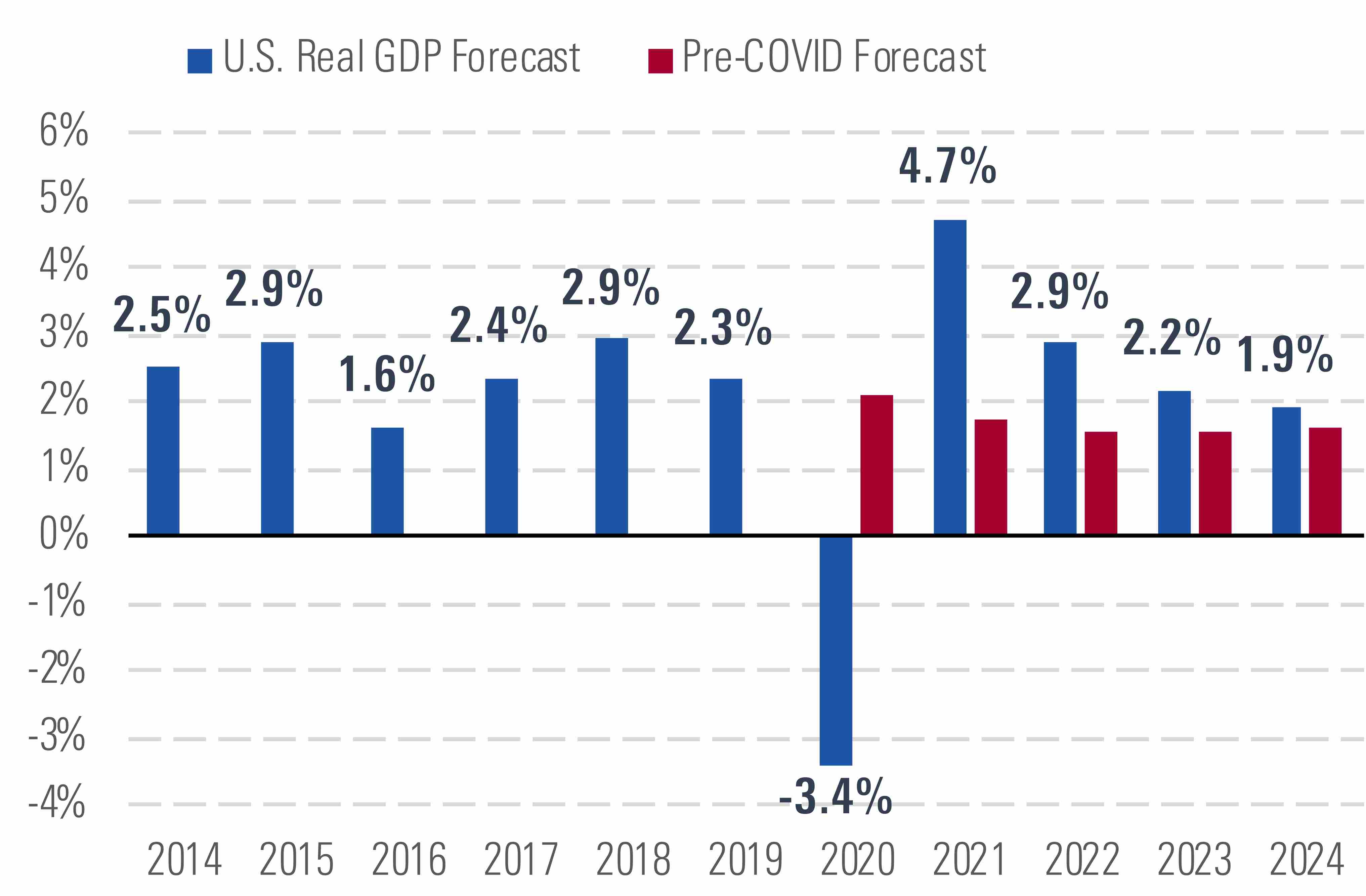

In the past six months, consensus expectations have essentially converged to our optimistic view on the U.S. economic recovery. We expect U.S. GDP to drop 3.4% in 2020 but surge back in 2021 and experience further catch-up growth in following years. By 2024, we think that U.S. GDP will recover to just 1% below our pre-COVID-19 expectation.

U.S. GDP will fall sharply in 2020, but we expect rapid catch-up afterwards - Morningstar

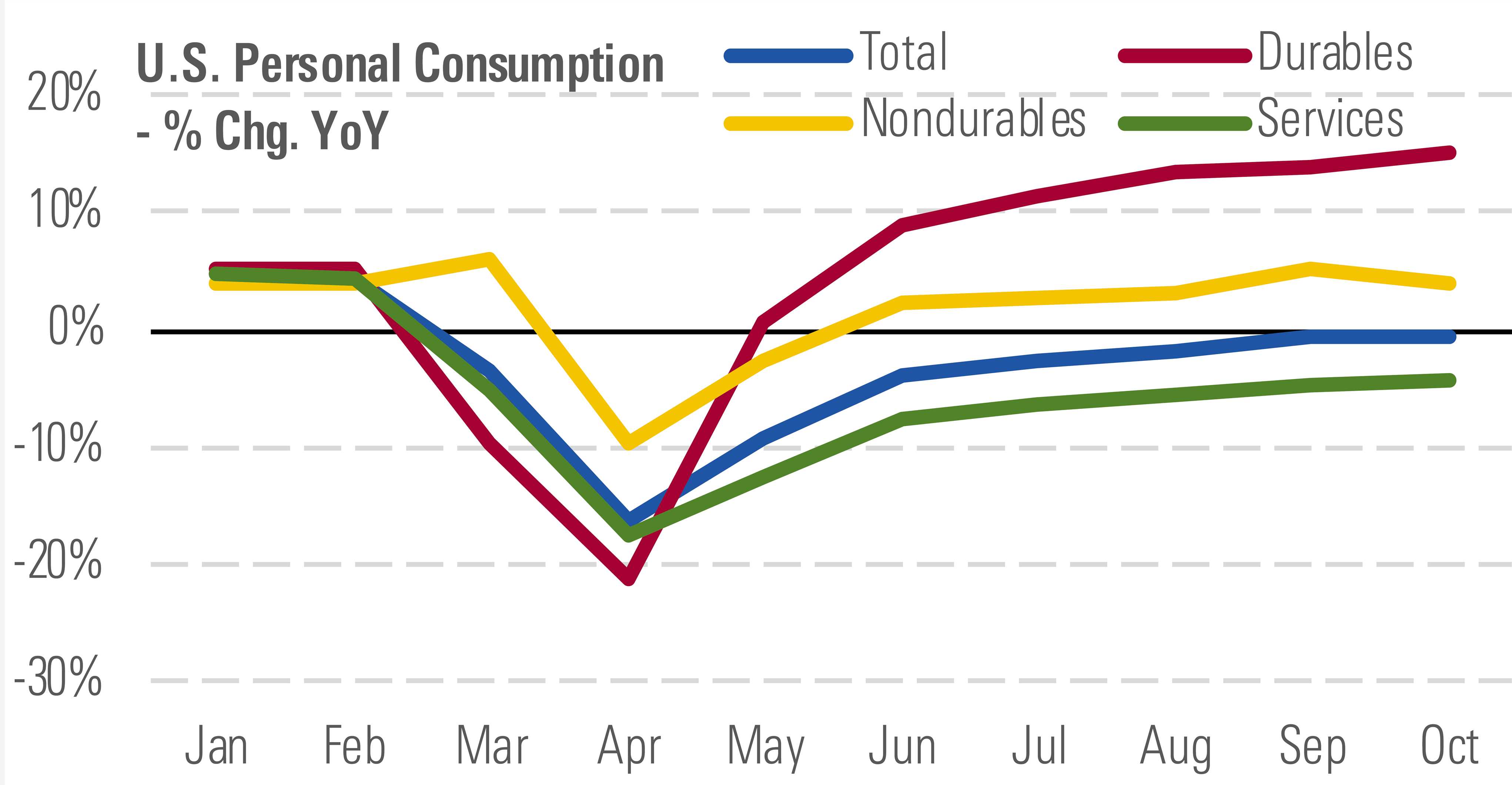

Widespread vaccination in the U.S. by mid-2021 should enable a return to normal in much of the economy. In industries highest affected by COVID-19 (such as restaurants and hotels), employment and output were down 15%-20% year over year in the third quarter. These industries account for just 6% of U.S. GDP at pre-pandemic levels but 15% of employment. As such, their recovery is critical for a broader labour market recovery. U.S. consumers are eager to spend, as evinced by very strong spending on consumer goods, especially durables. Consumer-services spending should come roaring back once the need for social distancing is alleviated by mass vaccination.

U.S. consumers are eager to spend - Morningstar

The passage of a new US$ 900 billion (about 4% of U.S. GDP) stimulus package has removed one concern regarding the U.S. economy. But we don't think a lack of stimulus would have been fatal to the recovery. Another potential threat is the surge in coronavirus cases in recent months; however, we don't think this will sink the economy before the vaccine can be rolled out. Additionally, we don't see major macroeconomic implications from the U.S. election outcome.

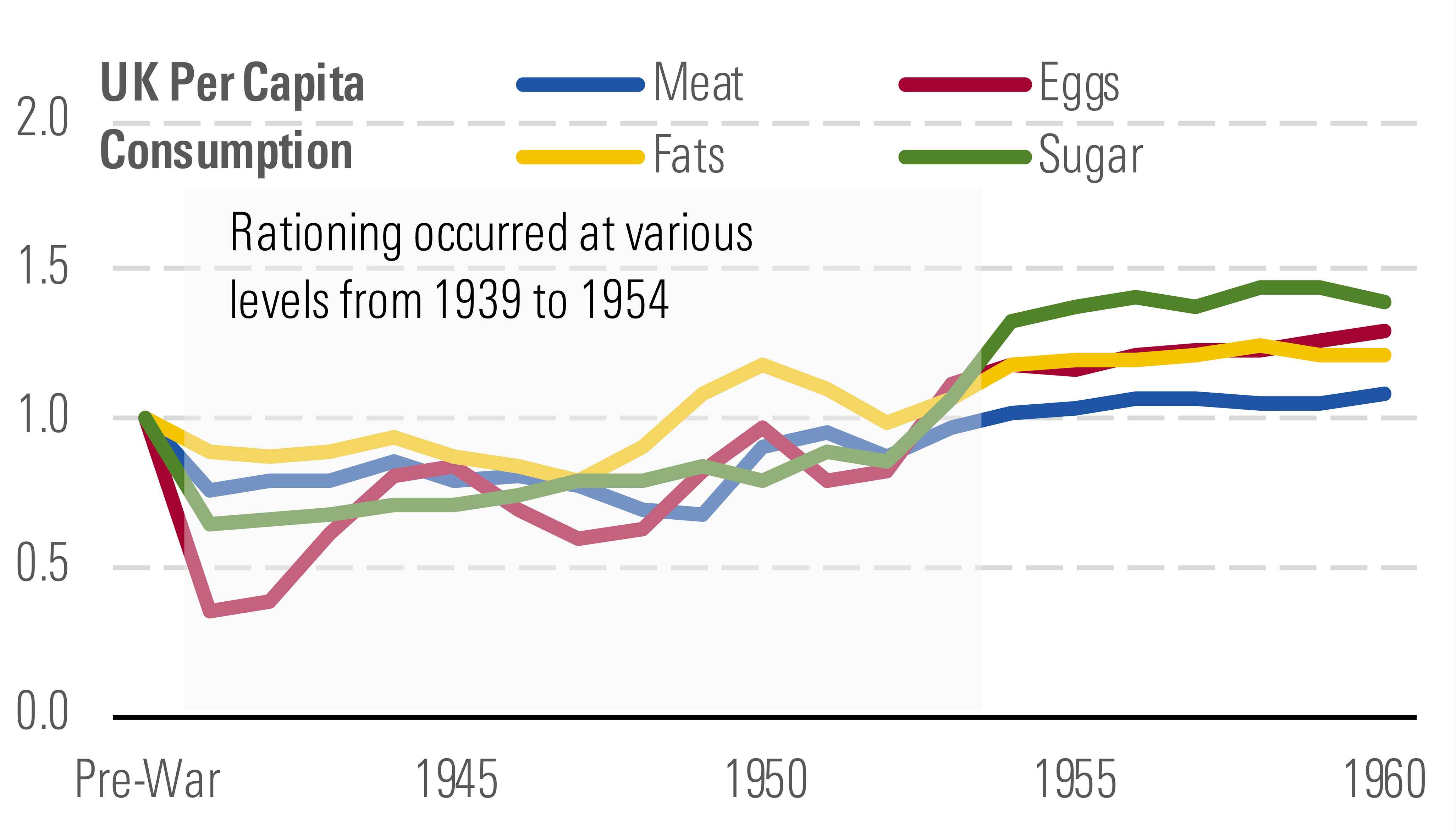

We've looked at several historical episodes in order to best understand the world after COVID-19. Our goal is to understand, in general, what happens when the economy is perturbed by an extreme but temporary external shock. Pandemics are one type of this class of events, but so also are wars, political upheaval, and related disruptions. For example, our analysis shows that U.K. rationing in World War II didn't depress long-run consumption of rationed goods via a change in habits. Instead, demand for rationed goods generally mounted a full recovery. Episodes like this suggest we should think carefully before proclaiming that any aspect of pandemic life will become the "new normal."

WWII rationing had little long-term impact on U.K. food demand - Morningstar

.png)