In part 1 of this article, we looked at what happened to value strategies in the past few years. In this part, we continue to explore whether value strategies have a comeback.

What’s Going on Now?

Value has bounced back, but it might be too soon to call it a comeback. From Sept. 1, 2020, through April 11, 2021, the Russell 3000 Value Index gained 30.52%, while the Russell 3000 Growth Index posted a relatively modest 14.39% return. Favorable stock exposure in the financials, industrials, and information technology sector explain much of the value benchmark’s outperformance over this stretch. Top stock contributors include a number of names that stand to benefit from the gradual reopening of the global economy following a year that saw most of the world locked down. These stocks include JPMorgan Chase (JPM), Disney (DIS), and ExxonMobil (XOM).

But while some are heralding a comeback, driven by a strong fundamental outlook for value stocks as the world gets back to normal, others are worried it may just be a junk rally. Take the performance of Invesco S&P 500 High Beta ETF (SPHB)as an example. The fund sweeps in the 100 S&P 500 stocks that are most sensitive to the market’s movement—a proxy for low quality. Indeed, the fund scores poorly on a number of quality metrics relative to those tracking its parent index. From Sept. 1, 2020, through April 11, 2021, SPHB outperformed iShares Core S&P 500 ETF (IVV)by 34 percentage points. Subpar stocks have posted above-average returns. There may be some merit to the argument that value’s comeback is a head fake.

Is Value Actually a Value?

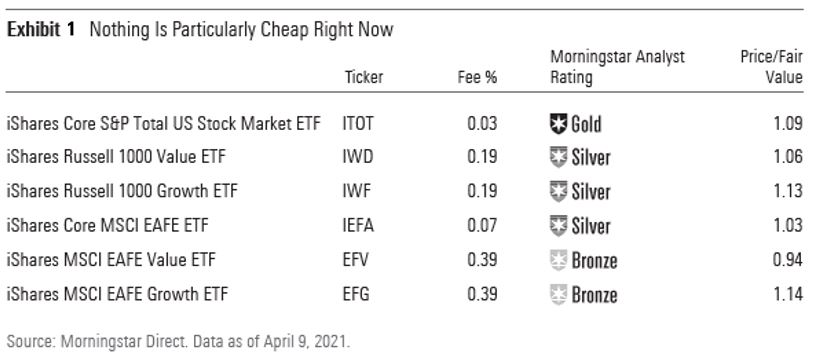

Whether value stocks’ run will continue is anyone’s guess. From the beginning of April through April 11, growth stocks had gained back some lost ground. What we can readily observe is whether there’s any value left in value stocks. Exhibit 3 features the Morningstar price/fair value estimate ratios for a selection of Morningstar Medalist exchange-traded funds that are good proxies for U.S. and developed international stocks as well as the value and growth camps in each of those markets.

No matter how you slice the U.S. market, stocks look more than fully priced. The trio of iShares Core S&P Total U.S. Stock Market ETF (ITOT), iShares Russell 1000 Value ETF (IWD), and iShares Russell 1000 Growth ETF (IWF)were all trading well above their fair value estimates as of the close of trading on April 9, 2021. While IWD’s price/fair value ratio was slightly lower than IWF’s, the value is only relative. Of the six ETFs featured here, only iShares MSCI EAFE Value ETF (EFV)was trading at a discount to its fair value estimate, albeit a slight one.

If there’s any value to be had among value stocks, investors are going to have to be choosy. As proxied by these ETFs and measured by Morningstar’s fair value estimates, value stocks, growth stocks—really almost all stocks—don’t appear to offer much value at the moment.

Is It Worth It?

After years of underperformance and anguish, many investors in systematic value strategies could rightly ask whether the juice is worth the squeeze. While any successful investment strategy involves prolonged periods of underperformance, value’s latest stretch has been especially long in duration and large in magnitude. The rebound in value stocks could mark the onset of a long, bright, warm summer. Or it could be a false spring. The only certainty is that seasons change.

There could be a lesson for investors in the long-term performance of the Russell value and growth indexes. From their December 1978 inception through April 11, 2021, the value index gained 12.09% annually while the growth index gained 12.11% per year. At face value, long-haul investors in either arrived at essentially the same destination. Late Vanguard founder Jack Bogle often made similar observations regarding the first value and growth index funds the firm launched under his watch. Of course, the path to these remarkably similar returns has been long and winding, and the figures are very sensitive to one’s choice of starting and ending points. But the point is that over a long enough time horizon, value and growth are essentially two sides of the same coin. Value stocks may or may not be cheap today. Growth stocks may or may not prove to have been a good value—despite sporting higher multiples—at some point down the road. As Berkshire Hathaway vice chairman Charlie Munger said, “All good investing is value investing.” Rather than flipping that coin at regular intervals, tilting between value and growth, most investors would be best served to own a total stock market index fund.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)