The trials and tribulations of stock markets are such that in observing short-term returns, there has been a fairly remarkable comeback. Over 12 months to the end of March 2021, global equities are up 39%, and while the UK has lagged with a 26.7% rise over this period, more-recent performance has started to paint a different picture.

If you think back to last year's volatility, it was airlines, oil, banks, energy, and cyclical parts of the market that felt the brunt of the downturn, while technology and disruption quickly started to appear as winners in the Covid-19 pandemic. As an investor, remaining calm was key, and if you were able to allocate capital, the “Covid trade” worked.

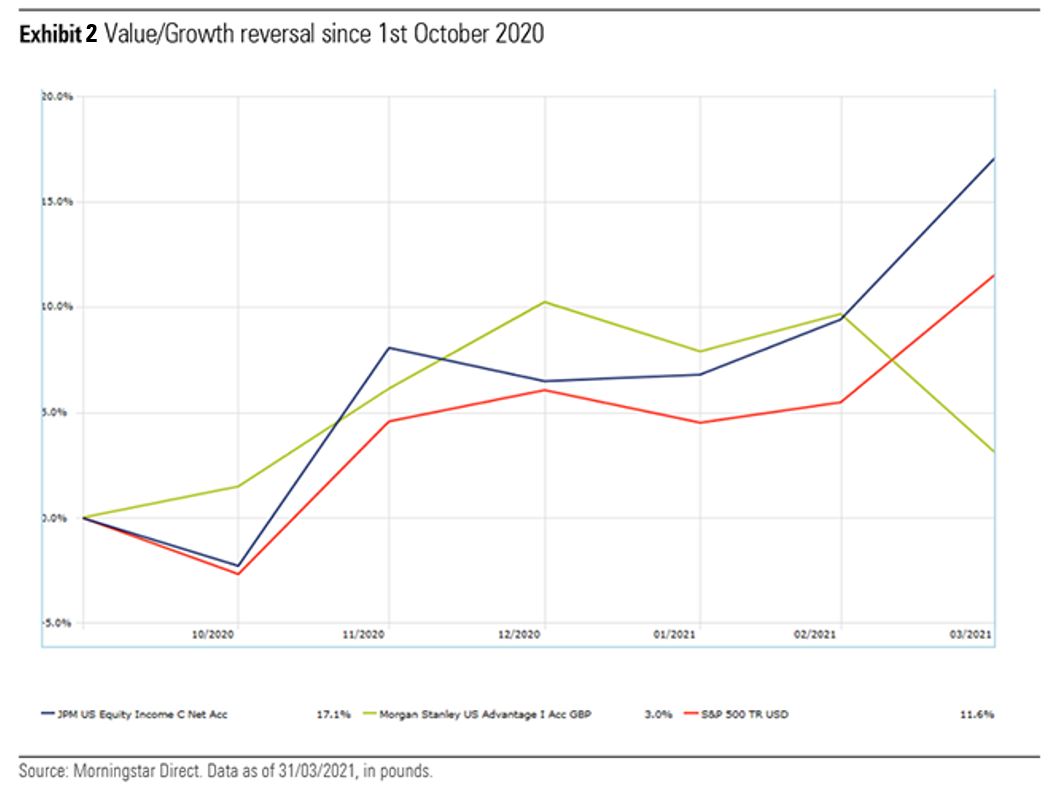

The following days and months saw sharp rallies in this part of the market, but that’s not been as clear-cut over the past six months. Indeed, with the market being forward-looking and a potential recovery in sight, plus trough valuations in cyclical areas, there has been significant outperformance from these stocks.

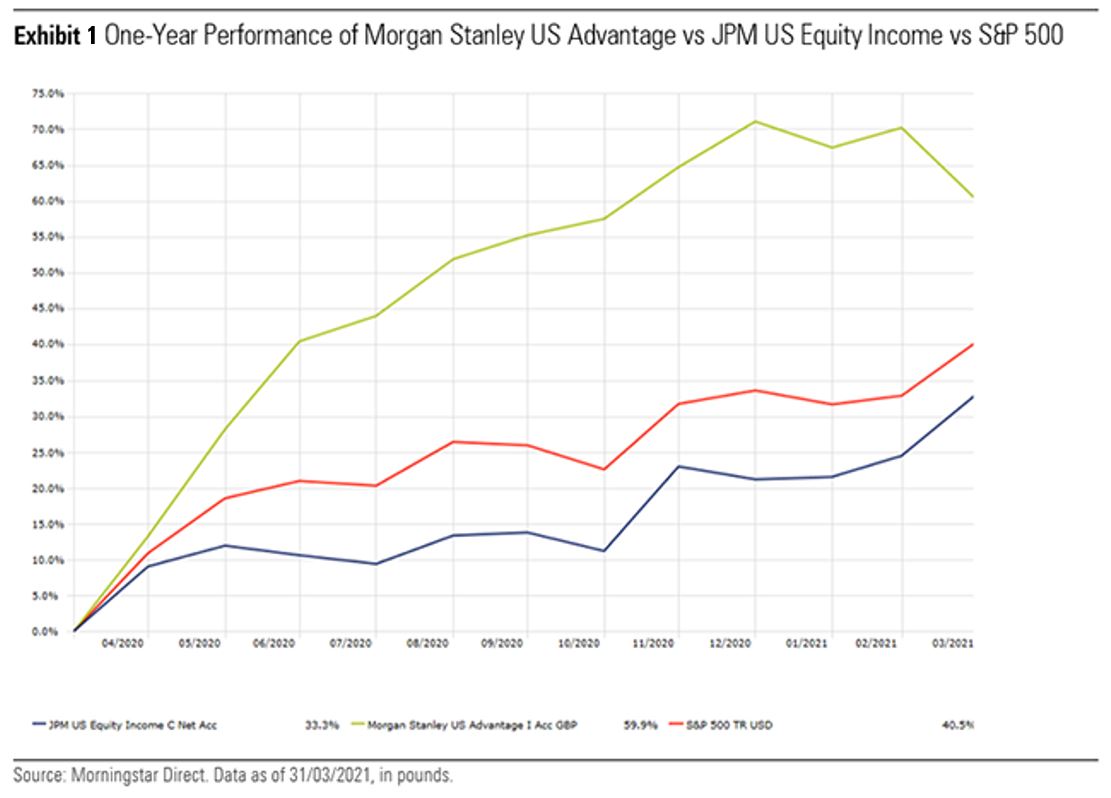

We can start comparing performance of US equities, the high technology weighting has been a boon to help drive performance and the sell-off was much shallower than some other developed markets like UK. Here we compare a US Equity Income strategy and Morgan Stanley US Advantage.

For the purpose of comparison, Gold-rated JPM US Equity Income strategy pays close attention to valuation, and in terms of style has a value leaning.

Silver-rated Morgan Stanley US Advantage, for sale in Hong Kong, is out-and-out growth. It focuses on established companies that are growing with enduring competitive advantages, such as solid brands, scale, network effects, or advantaged technology or intellectual property. Top holdings include the likes of Twitter (TWTR), Amazon.com (AMZN), Shopify (SHOP), Twilio (TWLO), and Spotify (SPOT). The extent to which these sorts of names motored as part of the “Covid winners” has resulted in a handsome outperformance over the past 12 months. The S&P 500 is used as a reference point in Exhibit 3 to capture the whole market, but the fund was still ahead of its growth comparator.

We would expect the JPM strategy to underperform the main market across this timeframe given its value bias, but what is perhaps not immediately obvious in the graph, is the extent to which the situation flipped in the latter part of 2020 and into this year.

More broadly, it’s not uncommon to observe funds that were top-decile over the past year, ending up in the bottom decile during the past six months. When turning to fund flows, as markets started to pick up in April and May 2020, it was evident that investors were backing previous winners whose structural tailwinds over the last five and 10 years were still in play--namely quality growth, technology, and disruption.

But being a contrarian would have also reaped rewards, and stronger ones at that, so far in 2021. Popular themes have been underperforming, and with inflation or even a cyclical uptick on the horizon, unloved areas have started to come back to the fore. While this doesn’t mean investors should necessarily overstretch in that direction, hanging on solely to the darlings of the past decade might not be prudent as part of a balanced portfolio.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)