In Part 1 of this article, we looked at how “sick companies” slipped into value strategies. In this part of the article, we will continue to explore value strategies.

Wonderful Companies at Fair Prices

Bernstein’s “sick company” metaphor is far from a panacea. Not all value strategies focus on dirt-cheap stocks with depressed outlooks.

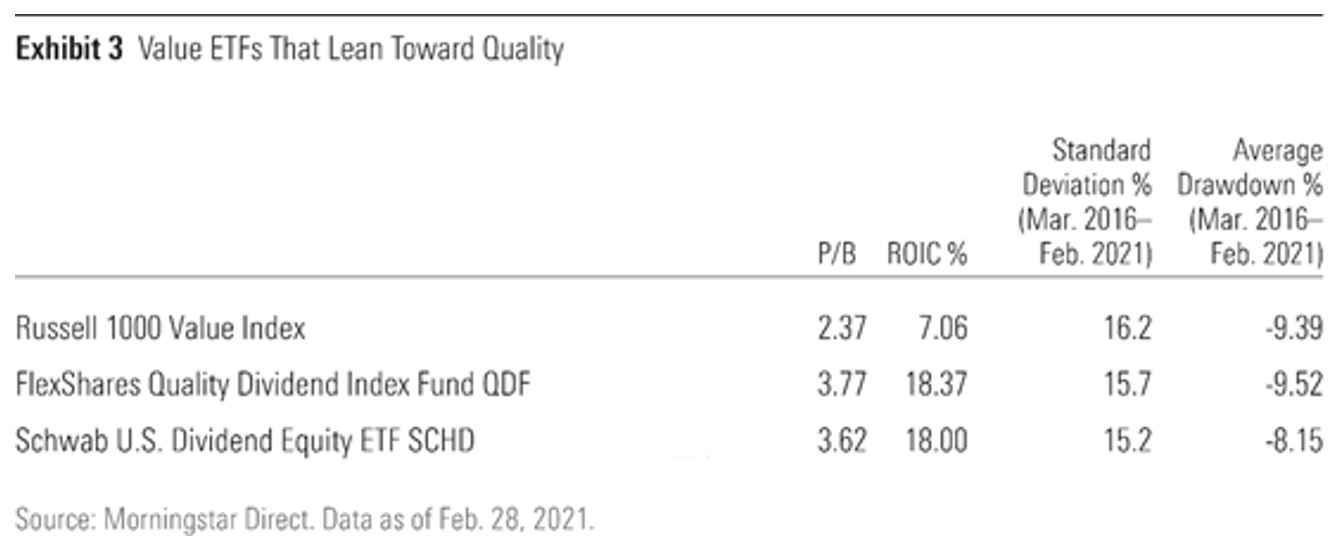

Funds at the opposite end of the value spectrum, like QDF or Schwab U.S. Dividend Equity ETF (SCHD), take a more-balanced approach and often hold shares in a number of more stable, profitable firms. Both ETFs screen for stocks with durable quality characteristics, then target names with higher yields than the market. Household names like 3M (MMM), Home Depot (HD), and Verizon Communications (VZ) are common holdings in both funds.

Large, mature companies such as these may not immediately come to mind when one thinks of value investing. They trade at higher multiples than the market, but their multiples are far from the most expensive. The reason has nothing to do with uncertain outlooks. Instead, these companies are often giants in their respective industries and face tough competition, meaning their ability to grow earnings at above-average rates is limited. Lower multiples can offset some of that tepid growth and facilitate reason-able performance. On balance, QDF and SCHD typically sport slightly higher average price/book ratios and higher-than-average profitability than the Russell 1000 Value Index, as shown in Exhibit 3.

The upside of these strategies is that they tend to be more stable than funds like RPV and SPYD. Their performance pokes along at a more timid pace, which is part of the reason they didn’t perform as well as RPV or SPYD over the past six months. But slow and steady is more likely to win the race--especially over the long term.

All Good Investing Is Value Investing

Systematic approaches to value investing tend to equate value with low price multiples. But value investing, at its heart, boils down to purchasing assets for less than they are worth. That definition is quite broad. It doesn’t rely on low multiples and has no constraints on time. Framed in that way, many investments, including those that trade at higher price multiples today, could qualify as value investments.

For instance, the S&P 500 closed at 1,468 on Sept. 30, 2000--the height of the late-1990s Internet bubble. At the time, its price/earnings ratio was above 27, considerably higher than its long-term average of about 15. From that perspective, the S&P 500, and funds that tracked it, looked expensive.

Fast forward more than 20 years to Dec. 31, 2020, when the index closed at 3,695. After three bear markets and countless drawdowns, the S&P 500’s price managed to grow at about 4.9% per year (the index’s total return was nearly 7% annualized over this same span). Over the same period, the collective earnings of these 500 firms compounded at a rate of 2.6% annualized. Few would question the observation that the collective value of these 500 companies has grown over those two decades. In hindsight, a fund tracking the index--even at eye-popping valuations--was by no means a bad investment. Good investments--those that inherently become more valuable over time--represent a form of value investing. From that perspective, you don’t need to own a value strategy to be a value investor. [2]

References

2. S&P 500 earnings growth figures were sourced from Robert Shiller’s website: http://www.econ.yale.edu/~shiller/data/ie_data.xls

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)