There are few consistent, long-term outperformers in the world of thematic funds. Judging the longevity of a theme can steer long-term investors away from speculating on various buzzwords.

Indeed, some funds appeal to investors because of their impressive, hefty returns, usually gained from a very specific trend over an extremely short period of time. For example, last year, tech themes rode on the demand created by the stay-home economy during the coronavirus pandemic. Many 5G operators, chipmakers and software developers were found relevant and thrived in the equity market. This favorable market brought eyepopping gains to tech-heavy portfolios. At the same time, more these kinds of fund products were made available. From May 2020 to date, 16 new funds were made available to Hong Kong investors, with 13 in technology, of which half play either new economy or 5G themes.

Not Many Survived

In the long-run, how many of these thematic funds even survive? Globally, the absolute number of surviving funds and proportion of outperformers out of the universe decease drastically year by year. The Morningstar Global Thematic Fund Landscape found out the success rate of thematic fund drops to just 22% of thematic funds when we look at the trailing 15-year period, and 57% shut down.

In Hong Kong, around 40% of thematic funds survived and outperformed. But is that a strong justification to invest in themes?

Of the 24 funds that were launched prior to 2011 and still exist, only Schroder ISF Global Sustainable Growth and BNP Paribas Funds Consumer Innovators beat the proxy Morningstar Global Equity Index on a 5-year and 10-year basis. And the latter is the only thematic fund that has consistently outperformed for the past 15 years. Outperformers are extremely rare.

Assessing Themes

So, how do we know if a theme works and over what time frame is the theme expected to play out?

Ben Johnson, director of global exchange-traded fund research, says investors can evaluate these funds by starting with a theme’s robustness. This requires data and judgement by thorough research.

1. Is the narrative convincing?

2. Is there a coherent and compelling growth story behind the strategy?

3. Is there data to back it up?

Johnson says: “A robust strategy should be loose enough to adapt as the specifics of the chosen theme inevitably evolve through time. As timely as they may seem now, some themes will age poorly.”

After gathering the fact and opinion of a theme’s fundamental strength (and weakness), the next step is to understand the key risk and return drivers embedded in the theme.

Johnson says: “Some extra risk is to be expected given the speculative nature and the narrow remit of many thematic strategies, but it also means they miss out on the risk-damping diversification benefits of broader equity holdings.”

He takes investing in a cannabis fund as an example. “It would be important to look beyond the growth projections and to fully understand the regulatory risks associated with that theme. Once isolated, it should be determined whether the risk and return drivers of the fund in question are either complementary or redundant when framed within an investor's portfolio.”

Knowing the Biases

However robust is a theme, there needs an execution. It is crucial that investors understand what the portfolios own. Below are the observations of thematic funds.

Size

At the time of writing, over 75% of thematic funds globally had a smaller size profile than the Morningstar Global Markets Index, a proxy for global equities. This is important because smaller stocks tend to have elevated risk profiles relative to their larger brethren.

Style

By their nature, thematic funds are trying to profit from areas of anticipated growth. It should therefore come as no surprise that more than 45% of these funds globally have a growth bias. This number rises to over 80% for technology-themed funds. Only 15% of all thematic funds had a value tilt at the time of writing.

The case of Hong Kong is even more extreme. About 70% of thematic funds for sale belong to either Large Growth or Mid Growth equity category defined by Morningstar style box.

Also, they commonly fall into themes such as disruptive tech, to hunt for the next Amazon or Google in the nascent trends like artificial intelligence, robotics and innovative mobility. Outside of tech, also with a large-cap tilt, the fund shelf abounds with sustainability, aging population and healthcare themes.

Sectors and Geography

One hallmark of thematic investing is a disregard for traditional sectors or geographies. Depending on the themes tracked, investment footprints can be strikingly different from broad global benchmarks like the Morningstar Global Markets Index. Portfolios with single-country or region also exist, with a narrower exposure that isolates Asia consumption and China healthcare.

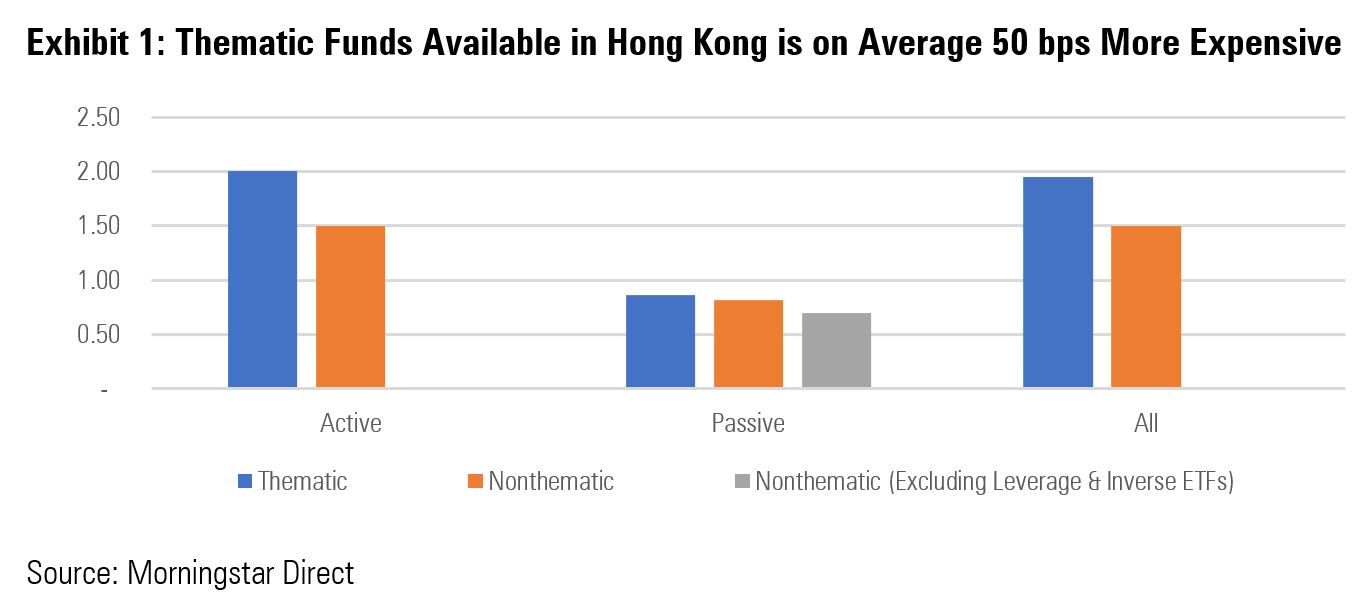

Fees

Thematic funds tend to be more expensive than their nonthematic counterparts. Across the 437 share classes offered in Hong Kong, thematic funds averaged an ongoing charge of roughly 2.0%. The fee difference is more pronounced in active funds, which is 50 bps more than the nonthematic funds.

But are they worth a higher fee? Fees have been shown to be the most reliable indicator of future fund performance. And authors of the Morningstar report also suggest that the higher fees can partly explain a lackluster long-term performance.

Picking a thematic fund that outperforms a low-cost global equity index fund over long-time horizon are stacked firmly against the investor in all regions. Because of their narrower exposures, thematic funds might be considered as single-stock substitutes for those investors looking to express a view on a particular theme but lacking the time, tools, and inclination to conduct due diligence on individual companies.

Johnson concludes: “Because of their narrow exposure and higher risk profile, thematic funds are best used to complement rather than replace existing core holdings. “The best themes are expected to play out over many years. This means that they are most suitably deployed over longer investment horizons.”

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

Have You Found Your Niche?

Explore the latest Global Thematic Fund Landscape report here

.png)

.jpg "Kate Lin")