Why is it important for investors evaluate pharma companies with non-financial standards? The idea echoes the question, ‘Why are pharma companies highly regulated?’. The actions of these companies impact humanity. Their products, services and research could -- directly or indirectly -- impact the safety of human beings, animals and the environment, both today and in the future, so every dollar you invest in these companies also reflects that.

At Morningstar, non-fundamental attributes contribute to ratings and valuations. Both the Sustainalytics ESG Risk Rating (corresponding to Morningstar's Globe Ratings), as well as Morningstar's equity research methodology, incorporate ESG risk into our valuations, uncertainty ratings, and moat ratings.

Large-scale drug makers in China are moving on from simple manufacturing to development. Domestically, they are incentivized by the government to launch research-heavy drugs like the treatment to control autoimmune diseases and cure cancers. Outside of China, BeiGene and Innovent Biologics, for example, were expedited by the U.S. FDA in their respective approvals for products curing cancers.

While Chinese pharma is growing into importance in the world’s medicine supply, it is currently exposed to a host of ESG-related risks that shouldn’t be ignored.

Potential Hazards

Social and governance are the notable ESG hotspots for pharmaceutical companies, according to Sustainalytics. Under the framework, medicine access, product governance and business ethics represent the material issues.

To be clear, we aren’t saying all drug makers are risky. In operating this business, companies are exposed to varying degrees of risk. They are individually assessed following Sustainalytics’ research methodology. To help evaluate each company’s risk, ask these questions:

1. Are their drugs safe to use?

In real life, drug makers rely heavily on distributors to reach a network of clinics and hospitals. It isn’t easy to spot if they promote moral sales behavior.

Moreover, you can browse online if their products report a history of unsafe features and unanticipated side effects. If this happens frequently, concerns arise from quality control and management. Also, you can tell from their marketing materials if they tend to exaggerate the actual effects or are deceptive in some ways. It is also ethical behaviour for drug makers to proactively recall products.

2. How are drug products being developed?

Conduct related to product development surrounds animal testing, stem cell research and clinical trials. Ethical risk is higher for companies involved in research and development that require testing on animals and humans, as well as for companies that outsource testing. Drug makers tend to make it public if they entirely or partially refine from animal testing programs.

3. Does a company intentionally make its products accessible and affordable, especially to lower-income countries?

Pricing, coverage by insurance policy and healthcare infrastructure determine a patient’s access to medical treatment. Allowing the production of cheaper generics without the consent of patent holders would greatly improve accessibility and affordability.

4. Is a company involved in bribery and corruption?

Bribery and corruption is an issue detected in the industry globally, especially bribery of healthcare professionals in return for prescribing company products and kickbacks. For companies making effort to minimize such risks, they would stop paying doctors to promote their products.

This is not a complete and permanent list, as ESG conditions are not static. They change over time, dynamically responding to each material decision made by company management as well as the evolving expectations from regulators and society. Investors should not omit the remedy a company puts in place after any incident, or preventive measures against a potential threat. The rule of thumb is always to judge with reasons.

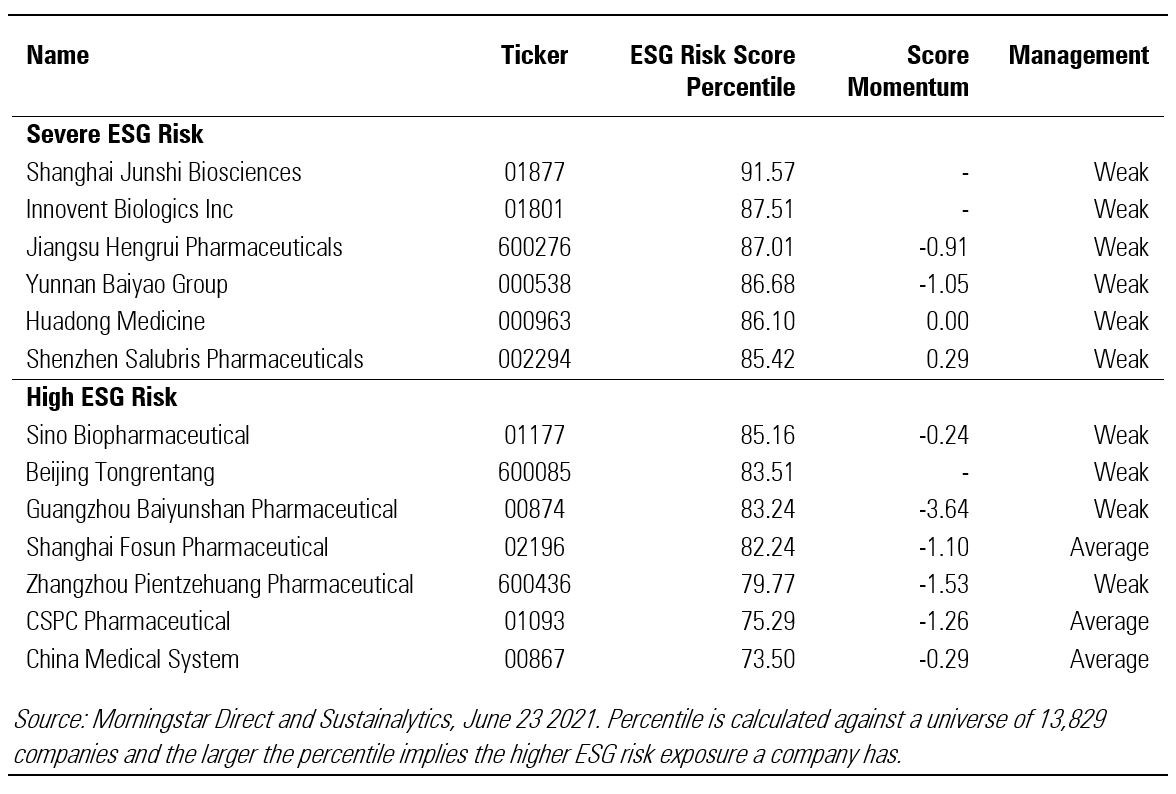

Measured by score momentum, the year-over-year absolute change in ESG risk score, most of the Chinese pharma companies show signs of improvement.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")