Big shifts in Chinese spending habits almost entirely explain why Alibaba (BABA, 09988), Tencent (00700) and JD.com (JD) have become among Asia's most valuable companies. After more than 10 years of explosive growth, internet businesses have begun to rub against each other. The market is concerned that regulation taking aim at these large players could impede their growth for the years to come.

But Morningstar analysts do not see challenges leading to a demise of the Chinese equivalent of the FAANGs. Chelsey Tam, senior equity analyst at Morningstar, says the growth engines that Chinese e-commerce leaders have today will still differentiate them from contenders for years to come.

1. Stable Cash Flow

Mega-scale internet companies run stable core businesses. They invested vast amounts of time and money building user bases, and thus network effects. Now those efforts are paying off.

The online marketplaces of JD.com and Alibaba's Tmall are mature enough to withstand strong competition. The business segments of these platforms will remain a major cash flow driver, according to Tam.

Tencent's flagship one-stop platform, which comprises payment, a social network and games, has a total of 1.2 billion users. Tam says the network effect is Tencent's economic moat source, providing a robust stream of advertising revenue. Sticky users and systematic monetization of activity are likely to preserve Tencent's economic moat for the next two decades.

2. Quality Focus

Platform-based players have been weighing the way they approach growth and profitability in this core segment. They look beyond the sheer size of the user base by putting a considerable emphasis on business sustainability.

In e-commerce, service quality is the most effective way to gain and retain loyal merchandisers and customers. Tam explains: "Merchandisers seek a predictable stream of sales, and customers need convenience and quality assurance. To fulfill both sides, good customer service is proved to be at the core of achieving client retention and repeat purchases." Citing its management, Tam says Tencent is comfortable committing capital to the online gaming business in order to pave a longer lifecycle for a quality games business.

3. Investing for the Future

Internet businesses are typically asset-light, but that doesn't mean they don't invest. Morningstar analysts have awarded Alibaba and Tencent an Exemplary Capital Allocation rating, which implies they have been good at channeling resources into profitable projects.

For example, Alibaba and JD.com have invested to improve the cost-efficiency of e-commerce business by strengthening their own homegrown logistics network. Tencent, on the other hand, pours resources into developing enterprise digital services to cater to the incremental demand among companies for cloud services and enterprise software, in particular in light of remote office needs after the outbreak of COVID.

4. Positioning for Untapped Markets

Online penetration in China still has room to grow and internet companies see holes to fill in both consumer and industrial markets.

Tam expects the individuals’ penetration rate to reach nearly half of the 1.3 billion population in the next decade, from the mid-20% level of 2020. One major growth opportunity is untapped rural areas through a new retailing model called community group purchase.

On the industrial side, Tencent is pioneering in the underdeveloped industrial internet. The firm's network effect plays out as it matches users with enterprises by transacting on Tencent's flagship Weixin payment platform.

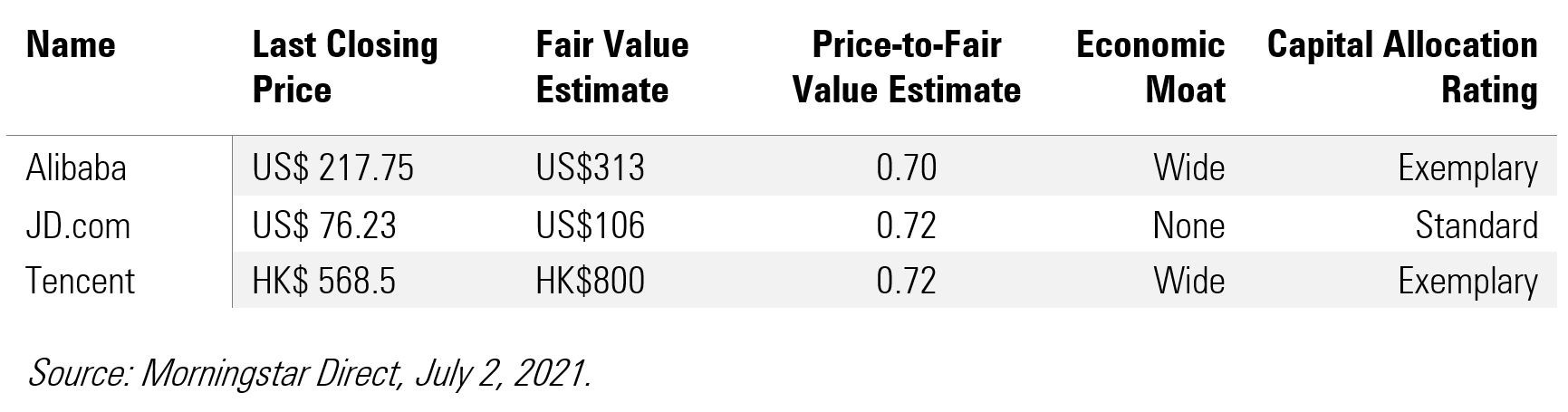

5. Undervalued Shares

Apart from growth engines to keep an eye on, the last reason that makes Chinese internet names a good long-term investment today is that they are significantly undervalued to fair value estimates.

Recent stock performance has been largely swung by negative sentiment due to the mainland's antitrust probe. The new raft of rules has turned the playground more favorable to smaller platforms like Meituan (03690) and US-listed Pinduoduo (PDD), also dragging investors' confidence in names with a dominant position in the market.

Tam remains steadfast in her view that regulatory headwinds do not deter the quality names from maintaining their market share and sees the recent pullback as an entry point to high-quality names. Also, a discount of at least 25% shall give investors a margin of safety.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")