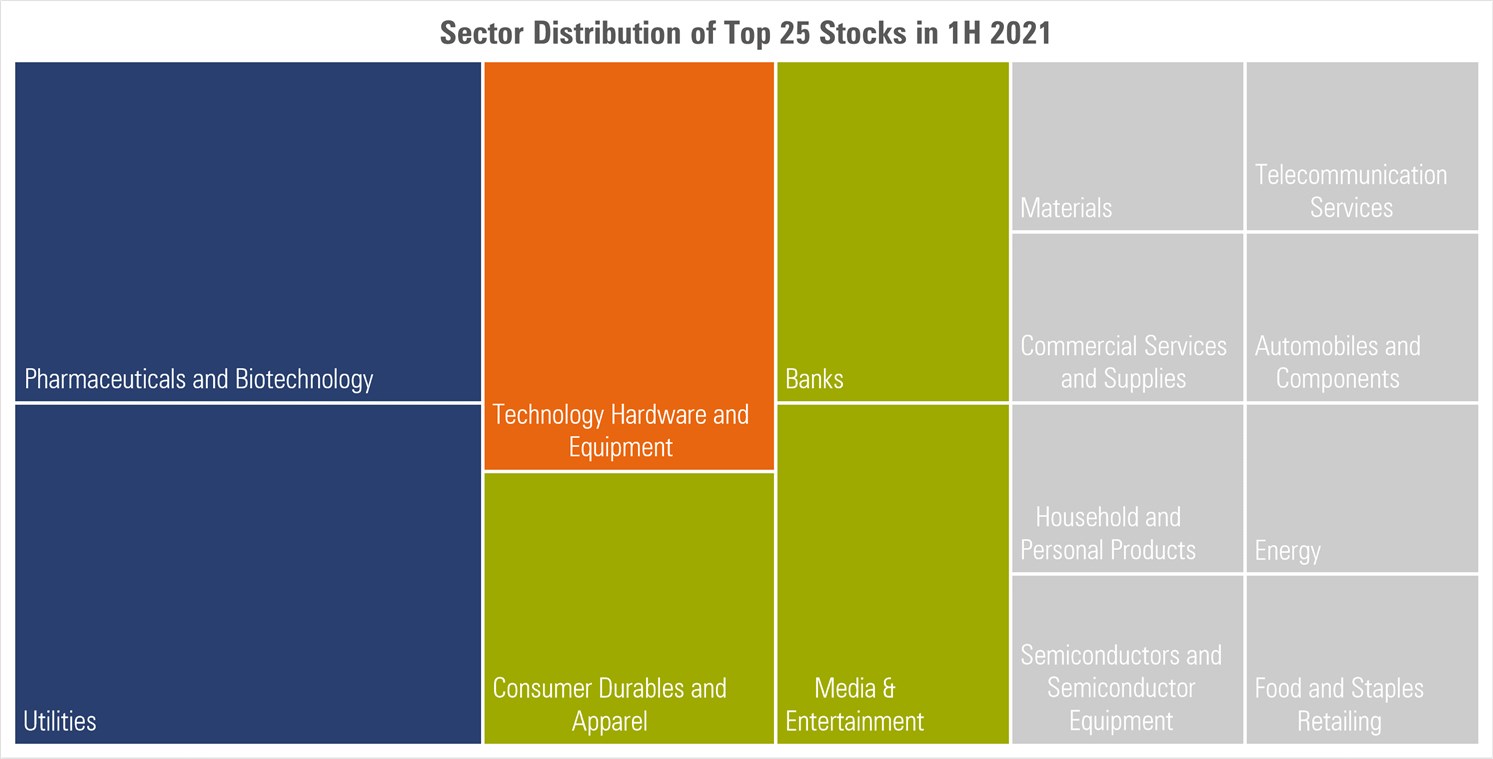

In Morningstar’s coverage universe of 300 stocks in Asia, excluding India and Japan, three sectors fill almost half the slots in the top 25 stocks by performance from January to June. These three sectors are pharmaceuticals and biotechnology, utilities, and technology (hardware and equipment). Here’s a look at the chart:

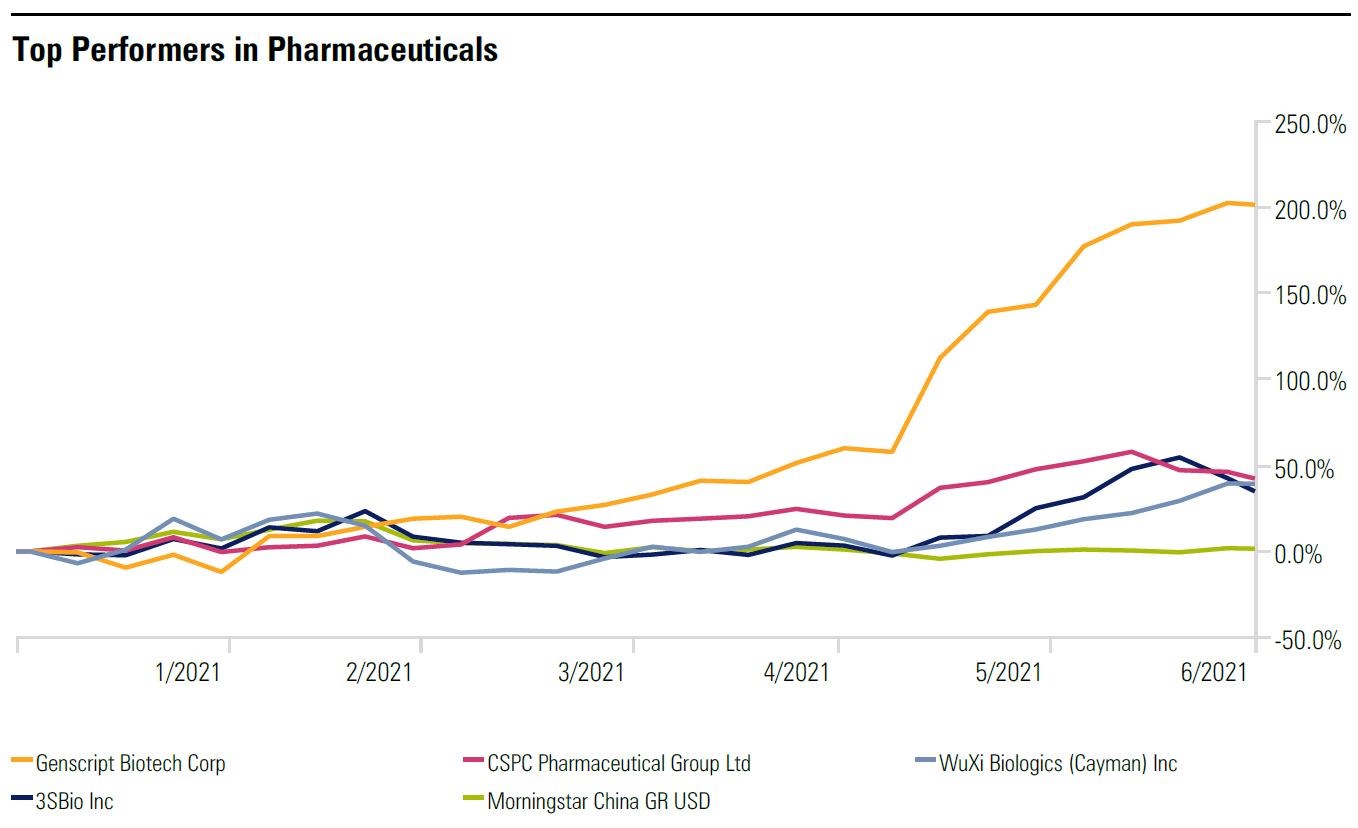

Biotech and Renewables

Genscript Biotech (01548) was the best year-to-date performer in Morningstar’s Greater China equity coverage, making a stellar return of 200%. The gene and cell therapy firm started 2021 with weak sentiment following an anti-smuggling probe by Chinese authorities on its management of human genetic sources such as organs, tissues and cells. The stock price recovered based on an investment by private equity fund Hillhouse Capital, which anchored much of investors’ confidence. The rest of the sector was buoyed by better visibility in outsourcing profitability, and an innovative drug pipeline. At the same time, the gains brought Genscript and Wuxi Biologics (02269) well above their respective fair value estimates by around 70%. However, these gains come with risks, as Morningstar analysts give the firms a Very High fair value uncertainty rating.

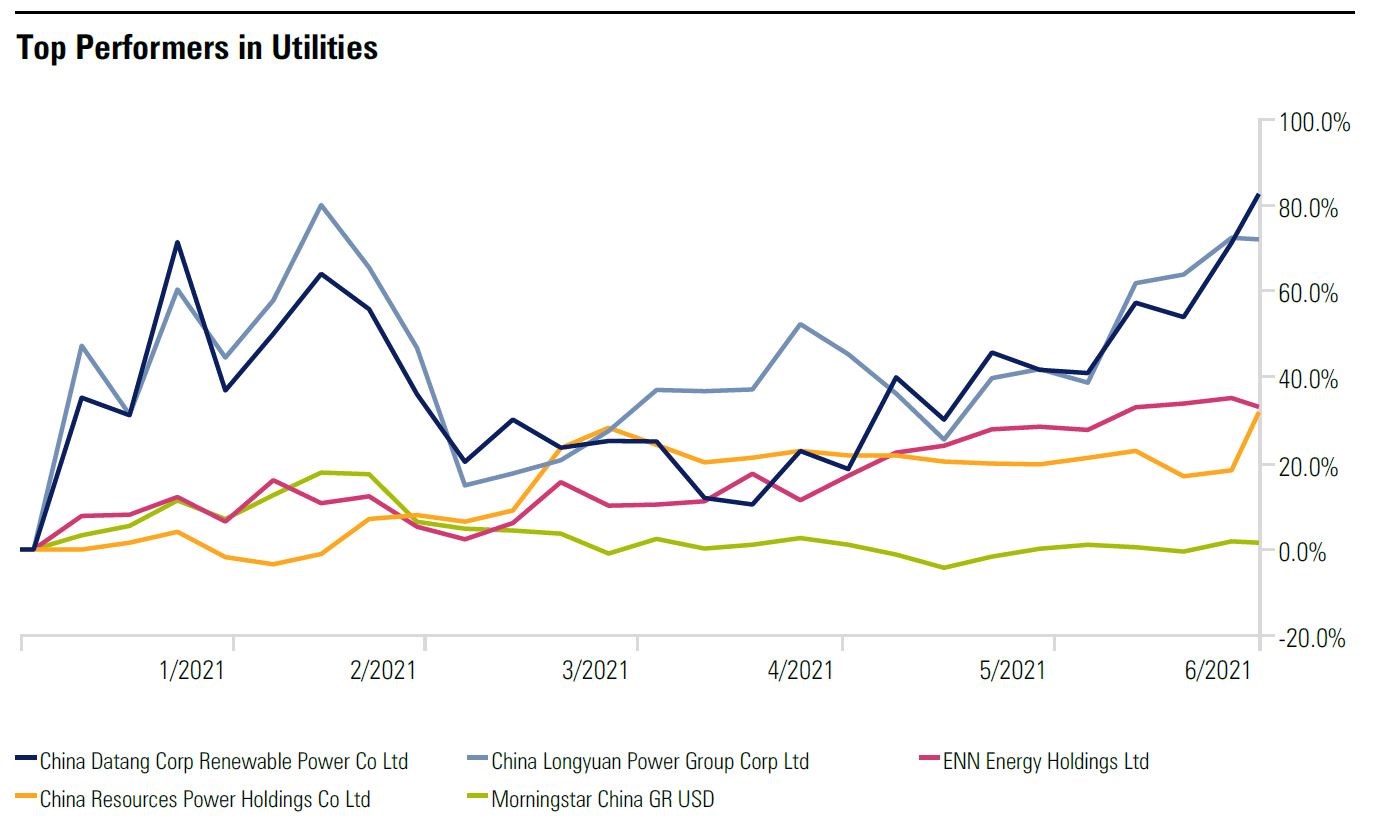

Another sector that outperformed others was utilities. Some companies in the sector clocked gains of more than 30% in six months.

A combination of macroeconomic factors and market sentiment contributed to the performance of energy producers on the mainland. As the Chinese economy continues to recover, especially in the manufacturing space, a surge in electricity consumption favors providers. Also, the floatation of China Three Gorges Renewables Group in June also drew investors’ interest in other ‘green energy assets’, for example wind power producer China Longyuan Power Group (00916).

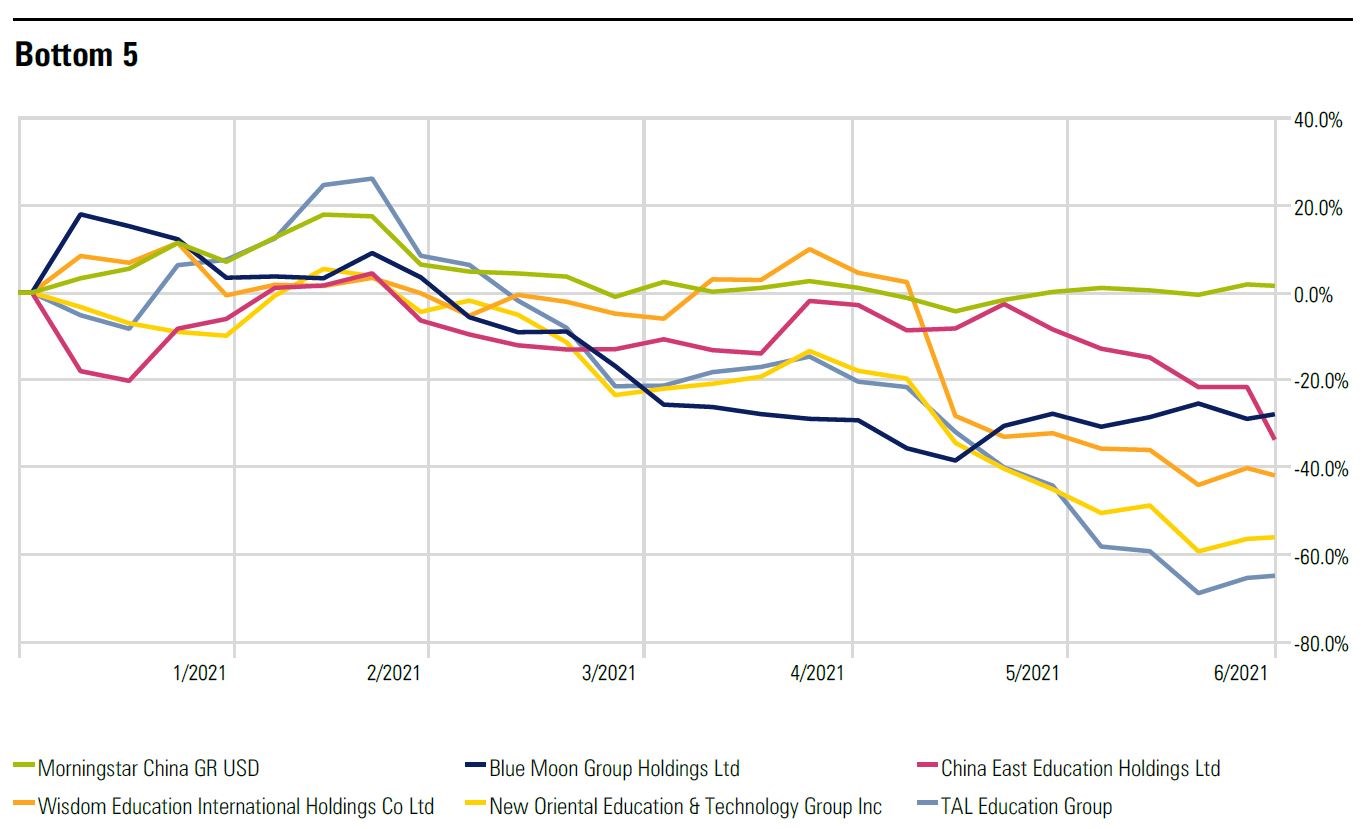

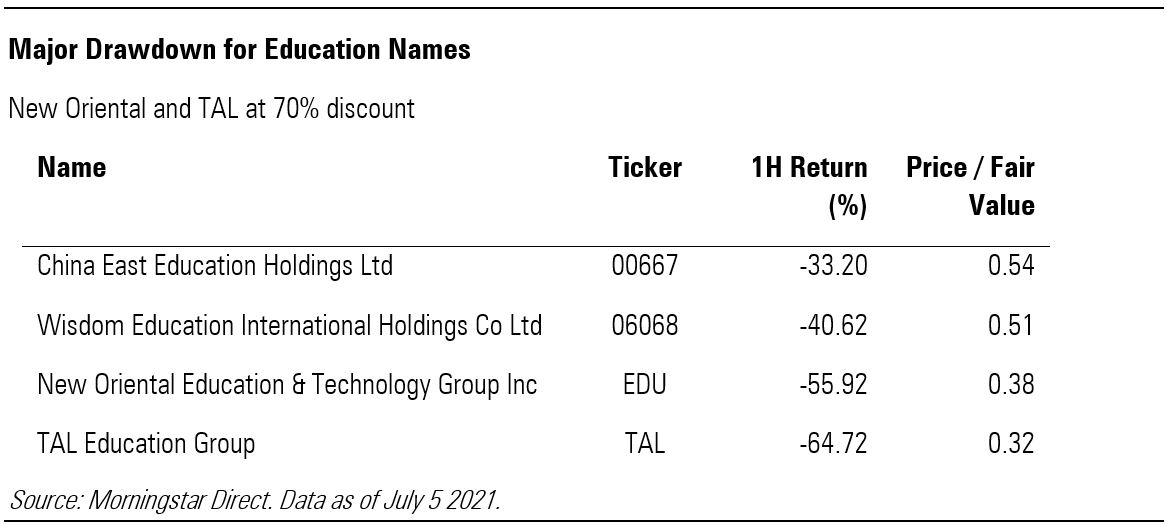

On the other hand, some trends emerge in the worst performers as well. Here’s a look at the bottom of the pile:

Morningstar senior equity analyst Jenny Tsai says the policy overhang explained much of the drawdown among the worst stock performances. In April, the Chinese government discussed a ban on excess fund raising, which put in a place a major impediment for the whole sector, which relies on capital raised via initial public offerings, or other channels. Mainland China education providers, listed either in Hong Kong or in the U.S., experienced a drop of at least 30%, with TAL Education hurting the most over a span of six periods.

The stocks’ fair value estimates remain the same as Tsai believes the market was overreacted over the talk. “We believe the China government will be implementing a set of policies to regulate the after-school tutoring industry to promote a healthier and transparent industry.”

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")