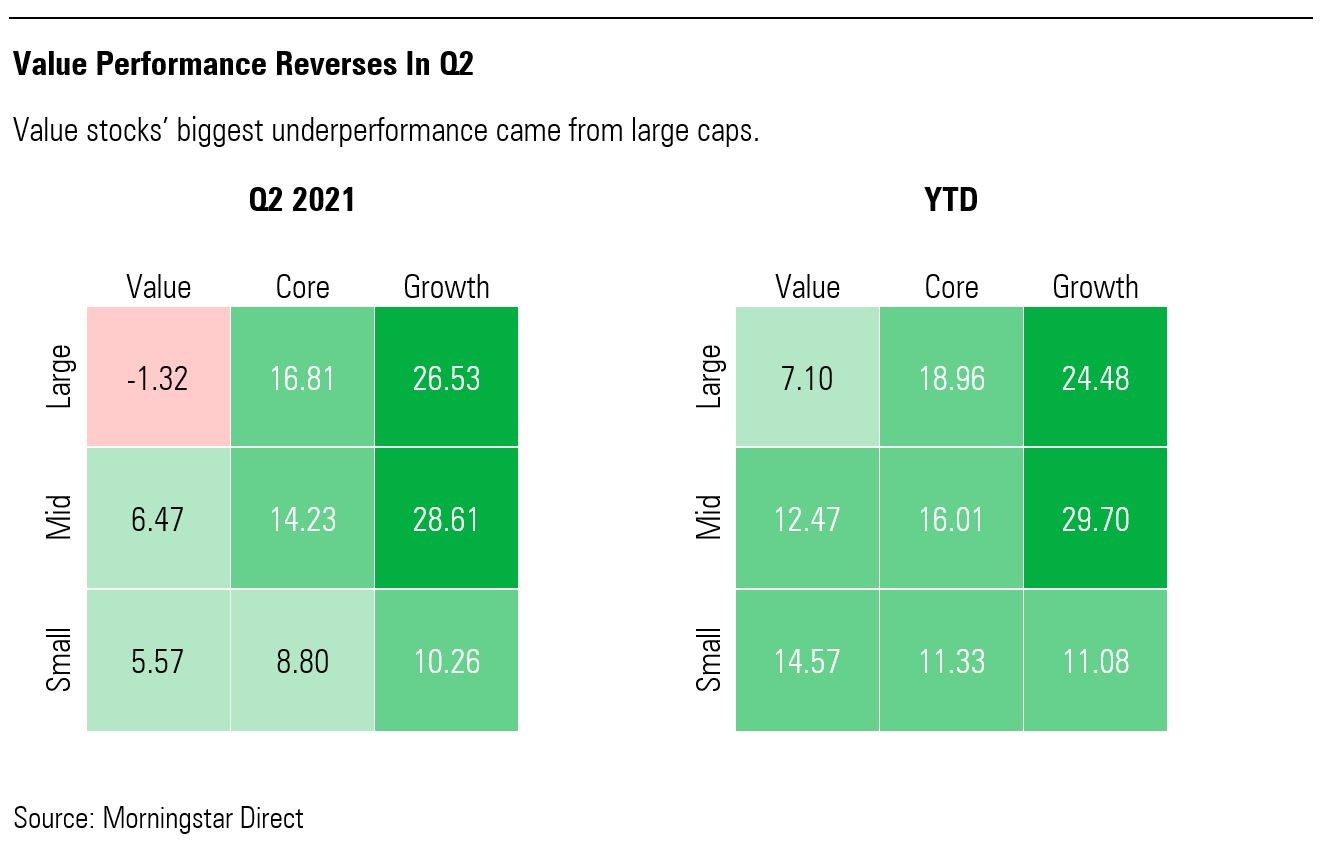

Year to date, on absolute terms, value-oriented stocks in China and Hong Kong markets have been not a bad place to be, delivering returns between 7% and 15% depending on market cap. This is a meaningful recovery from its weak performance for years.

That said, when compared to the core and growth buckets, value has underperformed since the beginning of 2021. Helped mainly by gains between April and June, growth stocks in mainland China and Hong Kong turned around to more than reverse a flat return in the first quarter.

Growth Again Outpaced the Broad Market

Large-cap growth stocks were back in spotlight in the second quarter. Nearly all categories performed better than the broad market. Technology, for example, outperformed by almost 40%. Category funds flipped the first quarter’s 8% negative return and gained 37% in this quarter. Large growth names in financial services, which consists of mainland brokerages, was the only sector that underperformed the broader market.

Equities that lagged during the pandemic began catching up as vaccines were approved and made available beginning in the fourth quarter of 2020. Between October and December 2020, small caps posted an impressive return of 20%, outperforming larger companies. Returns from value were also double-digit

Gains from ‘rotational trades’ markedly slowed over time. Investors of small-caps experienced gains ranging from 20% to flat. Value-tilted names ended the second quarter of 2021 with a 2% loss, contrasting with a 12% and 8% gain in the previous quarters.

Fairly-Valued, Be Selective

Moving on to valuation, our analysts believe companies in China and Hong Kong are priced fairly at the moment. This is because rotational trades have evened out valuation disparity between growth and value stocks and between sectors. The wide and clear gap of over- and undervaluation has disappeared.

“While Asia as a whole is not as expensive as the US market, trading at 4% premium to its fair value, the current valuation level presents a limited buffer to the downside,” says Lorraine Tan, Director of Equity Research, Asia for Morningstar, who believes a narrower margin of safety partially explains sideways trading in the market lately. Due to a smaller buffer against downside risk, the market has turned more vulnerable to negative news flow, which may result in significant equity flows in and out of the region, Tan says.

Heading into the third quarter, our analysts continue to see value in real estate, financials and energy. Tan says investors should stick to quality companies that command durable competitive advantage compared to industry peers. “We have to be selective for the rest of 2021, with a preference for those that are wide and narrow moat-rated companies as we think their very strong competitive advantages will withstand the pushes or headwinds that may come forward in the near term,” adds Tan.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")