The Chinese government top leadership has a non-exhaustive list of goals to achieve, so that it can realize its development master plan. Some of these goals relate to the biotech sector – grooming ‘truly innovative’ drug developers, making public health resources accessible and affordable, and protecting proprietary data derived from research.

National Assets

In guidelines released by the Center for Drug Evaluation, biotech companies were asked to stick to a “clinical value-oriented approach” for future clinical trials. Jay Lee, equity analyst at Morningstar, reads the draft for comment as the Chinese FDA’s way to call for better use of national resources – phasing from heavy investment in “me-too” projects to original research and development of oncology drugs. The former is defined as follow-on products that ride on mainstream and already known drugs. A majority of the prospective launches by Chinese biotech firms belong to this bucket.

Earlier this month, the country’s ruling party also cited in a separate document that it plans to actively work on law enforcement in medical services among other sectors, in order to respond to people’s growing need for a better life.

Lee, who covers the Chinese biotech sector at Morningstar, believes that the policy tone circles back to a broader plan that sets to achieve “common prosperity” – a term most recently used in Chinese President Xi Jinping’s speech on development, calling to look after those who are in need. Drug research and development leverages much on national resources, ranging from beneficial tax breaks and access to the hospital network for drug distribution. Reciprocally, authorities are seeking to generate higher social value with the resources granted to these privately-owned drug researchers.

Worth to Hold?

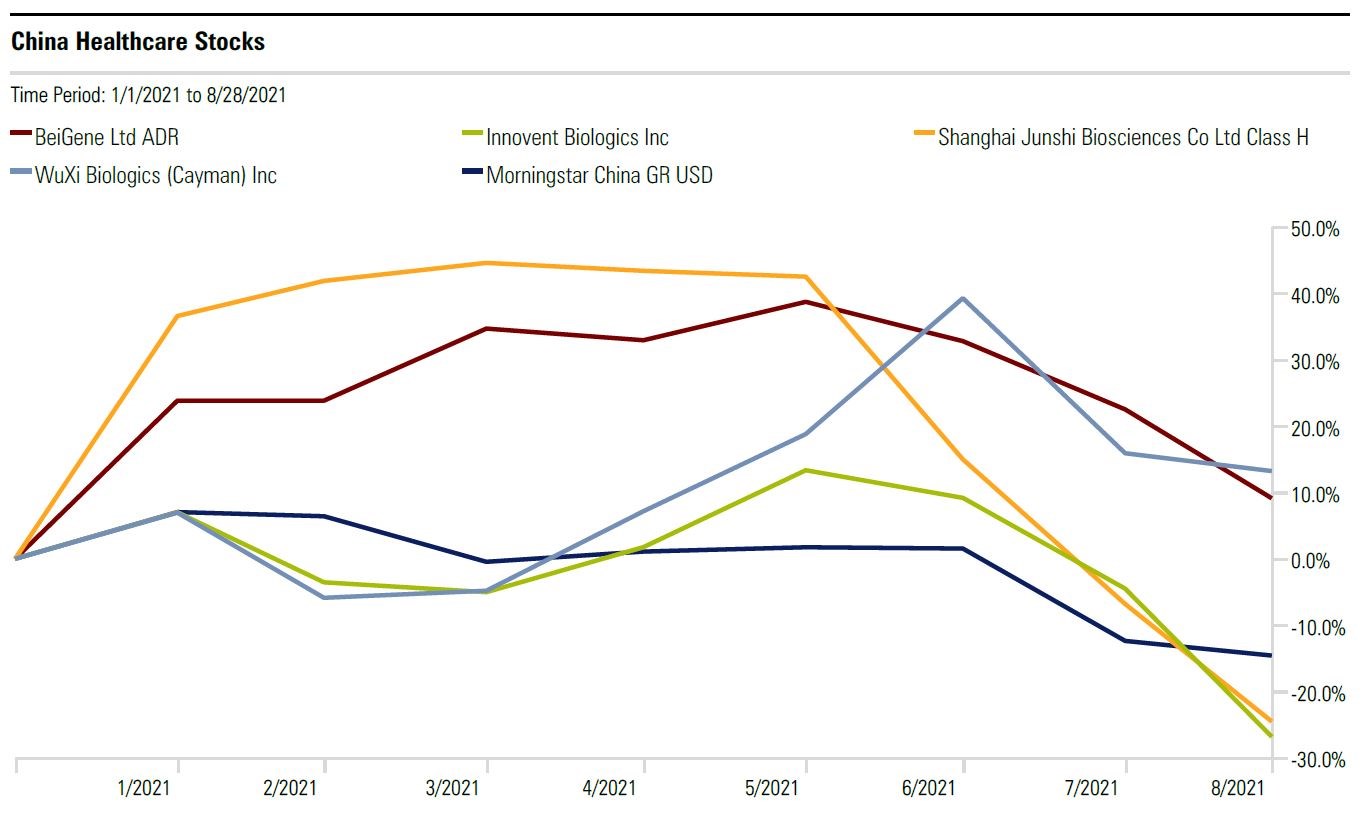

After the draft being published, among those impacted was WuXi Biologics (02269), which had a banner year in 2020 gaining over 200% in its shares. The firm is a contract development and manufacturing company (CDMOs). It partners with pharmaceutical companies manufactures drugs at a lower cost. Investors were concerned that the tighter rule will cap the profitability of WuXi Biologics and other CDMOs. In less than two months, WuXi slid 30% below its peak of US$ 145.6 reached on June 28.

“WuXi’s current projects are filled with developing less innovative biosimilar drugs for clients. At the moment, the timing for their clients to drop biosimilar and move onto innovative projects still depends on the clarity of rules and individual company’s pipeline. For now, there lacks the details and concrete plans that would suspend the tax break offered to the likes of WuXi or pull resources out of their existing projects,” Lee said.

Having said that, shares in WuXi Biologics hold up fairly well versus other Chinese biotech names. The stock rose 13% year-to-date even taking into account the July correction, far better than biotech names like Innovent Biologics (01801) and Shanghai Junshi Biosciences (01877). Instead of a capital exodus from the entire space, Lee foresees a higher likelihood of investors to move instead into WuXi from beaten-up names like Innovent and Junshi.

“Investors continue to view WuXi as a diversified way to enjoy exposure to China’s biotech industry, without being exposed to the volatility of individual biotech stocks, which arises from the binary outcomes of clinical trials, drug approvals, and coverage decisions,” Lee says.

Beyond WuXi

So what follows a bull rally for WuXi? Investors may also want to turn to other names to diversify. US-listed I-Mab Biopharma (IMAB) is one of Lee’s high conviction names.

He notes that I-Mab’s pipeline is more innovative than most Chinese biotech companies covered. “Its in-house assets have demonstrated clearer signs of differentiation in design and early clinical trial results. Additionally, its in-licensing strategy for the China market has generally focused on smaller, uncrowded spaces rather than huge crowded markets like PD-1 or biosimilars.”

According to Lee, I-Mab carries out forward-looking and cutting-edge partnerships and projects in addition to its outstanding innovative portfolio of differentiated candidates with global potential, including cancer cell inhibitors. These qualities earn it a positive trend to improve its lack-of-moat situation today. Another plus for the stock, based on Morningstar equity research, is that it is trading with a 50% upside to the US$ 95 fair value estimate.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")