Chinese investors have been watching the China Evergrande Group (03333) situation with increasing worry for a while now. In the latest twist, the real estate developer is on the edge of defaulting on its massive bond complex. The indebted developer’s website says it owns more than 1,300 projects in more than 280 cities. It also has around US$300 bn in liabilities.

“While official estimates of NPLs and special-mention loans are at 5.5% of GDP (in China), private sector estimates are significantly higher... Risks within the real estate sector are also rising: the liquidity crunch facing China’s largest property developer Evergrande Group is emblematic of the problems within the sector. Real estate and construction account for a quarter of fixed asset investment, 20% of banks loans and 15% of GDP,” said a DBRS Morningstar report.

While the stock price has fallen close to 80% year to date, investors are now shifting focus to the possible spillover effect on sectors and companies with links to the overall Chinese property market, like the banks.

The Most Impacted

Since mid-2020, China's ’Three Red Lines’ policy, designed as a state-wide initiative to manage systemic risks stemming from the indebted property development sector, has been in effect. It uses three thresholds to evaluate a real estate developer’s borrowing level for the following year:

- a 70% ceiling on liabilities to assets, excluding advance proceeds from projects sold on contract,

- a 100% cap on net debt to equity,

- a cash to short-term borrowing ratio of at least one.

Even if a firm passes all the requirements, it can only borrow an additional 15% in debt volume in the next year.

One year later, some of the most indebted real-estate players, like Evergrande and Guangzhou R&F Properties (02777), are under stress. When a real estate developer melts down, their funding banks will have to register the unsettled loans as bad debts. While the bad debt level rises, to meet the regulatory requirement, the involved Chinese banks will have to set aside a larger provision that allows them to cover 150% of the non-performing loans

Across her banking coverage, Iris Tan, identifies a few names that are more vulnerable to the current situation than the others. The exposure of China Minsheng Banking Corporation (01988) and Bank of Communications (03328) to property developers is the highest, she says, adding that in the unlikely scenario of the non-performing loan ratio rising to 10% of the total loan, the profit impact for CMBC and BoCom will be a decline by close to 40% and 120%, respectively.

Ping An Bank (000001), Bank of China (03988), and China Citic Bank (601998) will face lesser pressure, with a single-digit drop in profit if they were to top up the provision for bad loans. For the well-provisioned banks, Tan does not expect any impact on profitability even if non-performing loans for property developers are at 10% of total loans.

Tan adds that the risk of a sharp increase in the non-performing loan for banks within one year is a very low probability event. Other than provision coverage, variables she considers include higher property lending exposure, lower profit margin, and a bank with a lower NPL ratio. These will ultimately decide the negative impact on profits.

“In all likelihood, our estimates may overstate the risk as we don't have clarity on [the level of provision] that is already provided for in terms of real estate exposure,” she says. The flow-on impact to the financial institutions under Morningstar’s coverage is expected to be limited.

Managing the Caps

At the beginning of 2021, banks had to readjust their exposure to commercial and individual property loans from a total loan perspective. Depending on the scale of the lender, the upper limit of the commercial loan proportion in the book must be between 12.5% and 40%. A bank can hold 7.5%-32.5% of loan assets in an individual mortgage.

This percentage cap goes hand-in-hand with the three-threshold restrictions placed on property developers. But the rules aren’t an apples-to-apples comparison. Tan explains: “Even before this specific cap, banks took a rather prudent and selective attitude on property loans over the past few years. Exposure to developer loans always remained below 10% for most banks.”

For banks in our coverage universe, China Construction Bank (00939) and Postal Savings Bank of China (01658) are now above the mortgage cap, while China Merchants Bank saw its exposure surpassing both caps on mortgages and total property loans.

“Banks that do not meet the requirements are granted a grace period between two and four years, which is adequate for them to settle the outstanding loans with an imminent maturity and manage the line-up of new loans while preventing a breach of the regulatory limit.”

The reasonably long transition period would seem to soothe the negative impacts between today and the deadline. This adds to the estimation that the overall market loan growth remains strong at over 12%. Therefore, banks will have enough growth elsewhere to recoup the net interest margin they are will sacrifice in the property loan space, according to Tan. The risks have also been more than reflected in the current valuation and she thus concludes that the recent selling of bank and insurer stocks on exposure concerns is overdone.

Popular Asset Class

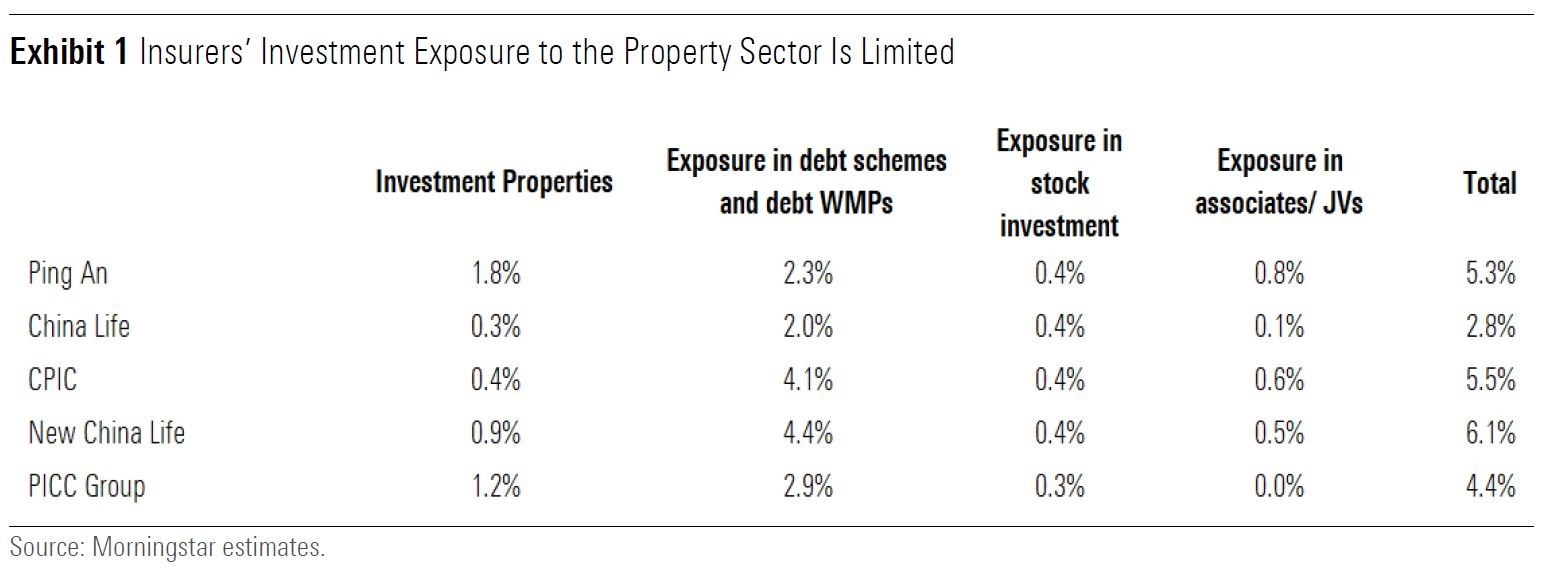

The case for Chinese insurers is slightly different, as their exposure to property developers comes mainly from their investment books. Real estate has become a popular investment for insurers, because it is one of the few sectors that give out stable yields and match insurers’ long-duration liabilities, especially in this low-interest rate environment.

Insurance companies under Morningstar’s coverage have a manageable exposure toward the sector, ranged between 3% and 6%. Among the five covered insurers, China Life has the lowest exposure as its allocation to investment properties and non-standard credit asset investment is the lowest among peers.

Tan says: “Strong return on equity and a robust capital position will be the core strength for healthy Chinese insurers to defend themselves from the current market situations. Even if there is some uptick in write-downs if property market risk increases, we believe the risk of capital replenishment is low.”

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")