Few had foreseen the 2020 pandemic, that raised demand for physical goods and triggered electricity shortages. Investors interpret it as a challenge to China’s preparedness for clean energy. However, a value investor at T. Rowe Price sees long-term opportunities in energy, especially the transition to carbon neutrality.

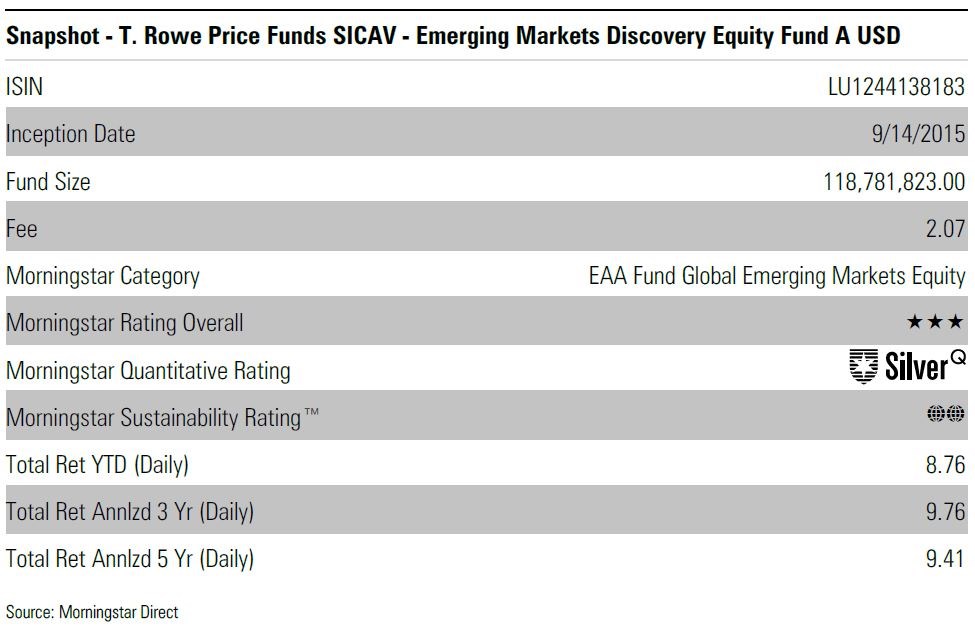

Ernest Yeung is a portfolio manager for the Emerging Markets Discovery Equity Strategy at T. Rowe Price, which earns a Morningstar Quantitative Rating of Silver. He believes that carbon offset projects in China and the broader emerging will present value opportunities.

Eureka Moments

Yeung says there’re two notable driving forces bringing carbon reduction to the forefront. First, from the top-down, G20 countries and the OECD have put precise goals in gradually lowering carbon emission. Yeung says: “The tangible carbon indicators detailed by a coal-dependent country like China was never heard of, and from which we feel China’s willingness to transit their energy mix, while carefully managing their sprawling coal industry value chain.”

The second is social media. While Gen-Z and millennials stay home during the lockdown periods, social media has become indispensable.

“With solid direction, investors are able to work the numbers backward,” Yeung continues. “So, people have started examining how, to achieve carbon neutrality by 2060, there will need to be a certain number of resources allocated to wind and solar energy. Investors have flocked into these sectors, hoping to ride on a trend that’s deemed irreversible by many.”

He says the discrepancy before and after countries announced a clear carbon reduction roadmap was impactful and presents a steeper expected growth curve. “The very first stage of reactions by the market, as we have seen in the past months, was buying names that would directly participate in this shift, like wind and solar farms and electric vehicles. We think these are already discovered names and an overwhelming optimism makes some of them overvalued.”

Value Approach

For years, the perspective on value stocks has been negative as it did not offer returns as compelling as those of growth stocks. “We understand that the market feels that the old economy will continue to be challenged and replaced by newer technologies. We don’t rush in just because they have value characteristics.”

In many aspects, though, Yeung holds on to his contrarian value belief. “Speaking of risk and reward, the market should not be so bearish with value.” He adds the needs in the real world have reemerged and will unlock a runway for value investing that would last at least a decade. The Emerging Markets Discovery Equity Strategy under Yeung’s management loads up with names that are an enabler of a green economy transitioning

“Despite the thriving tech scene, commodities and mining are still relevant. They are necessary inputs to build the infrastructure that enables the transition to clean power.”

While these names enjoyed a ride amid a value rotation at the beginning of 2021, Yeung believes the valuation metrics still look relatively rational versus some of the pure renewable plays. In his portfolio, basic materials, energy, and industrials each take up 8% of assets. He says he has selectively added to the names as prices correct.

Capex Cycle

Yeung also thinks the green economy development will require a massive scale of financing and is hopeful that would open up a new business area for the banking sector. “Project financing and capital expenditure for different infrastructure developments will bring back corporate banking’s growth story,” he explains.

“Globally, retail banking was the powerhouse of banks for the past 10 years. Take China as an example, from 2000, it kicked started an investment supercycle. Only after Lehman Brothers collapsed, China and many countries realized that they overinvested. The world took more than 10 years now to digest the oversupply.”

According to Yeung, the nascent development of green infrastructure in many of the emerging markets is likely to turn into a long cycle of capex expansion.

This theory is reflected in his investment preferences. The biggest portfolio overweight is in financial services, around 30% of portfolio assets invest in banks operating in the emerging markets, versus the category’s average of 20.7%. Sberbank of Russia (SBRCY), Hungry’s OTP Bank (OSZG), Saudi National Bank (1180), and India’s ICICI Bank (ICICI) made to the top 10 holdings at the end of September.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")