Investors will remember 2020 as a challenging year for dividends. By our count, more than one third of the dividend-paying companies in the Morningstar Global Markets Index, a broad gauge of developed and emerging markets equites, reduced, suspended, or eliminated shareholder payouts as the pandemic battered the global economy.

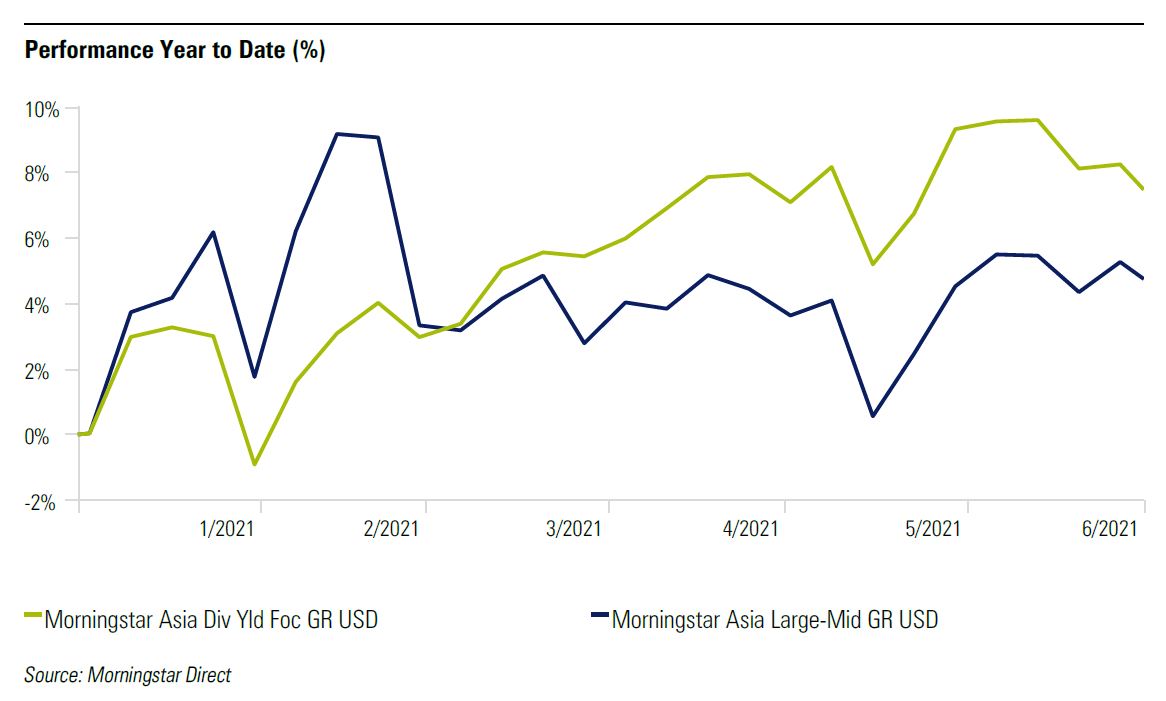

But with economic recovery has come a resurgence in the equity income segment of the equity market. The Morningstar Asia Dividend Yield Focus Index, which highlights dividend payers across the region, has recorded a strong year nearing the midpoint of 2021. The dividend index has gained more than 15% so far this year in USD terms, compared with 9.7% for its parent index, the Morningstar Asia Large-Mid Cap Index.

Investors who stuck with dividend payers have been rewarded—not just from a total return perspective but income as well.

The Equity Income Roller Coaster

In Asia, dividend payers posted far stronger total returns in 2020 than in other markets, but they still underperformed. The Morningstar Asia Dividend Yield Focus Index advanced 9.3% in 2020, compared with a 21% gain for the Morningstar Asia Index.

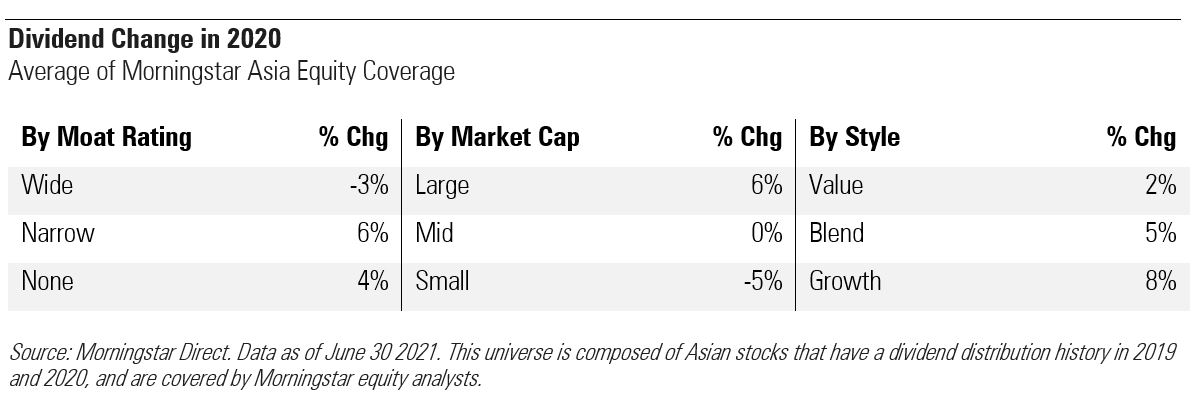

Many stocks across Asia cut their dividends. Energy companies like PetroChina, Korea’s S-Oil, Petronas of Malaysia suffered from falling demand a price war among oil producers. Basic materials stocks, such as Nippon Steel, China’s Baoshan Iron & Steel, and Thailand’s Indorama Ventures were impacted by economic downturn. Consumer stocks like Honda, Geely, and Hyundai Motors, Mandarin Oriental, and China’s ANTA Sports Products were hit by falling demand. Financial services stocks, such as Orix, Malayan Banking, Singapore’s United Overseas Bank, and Hong Kong Exchanges and Clearing saw plummeting business.

Though some technology companies cut their dividends too, the sector overall benefitted from a new normal of work from home, shop from home during the pandemic. Some big tech winners, such as Taiwan Semiconductor and Samsung Electronics were in the dividend index. Others like Tencent were not. The dividend index also suffered for not including such pandemic winners as Meituan, Pinduoduo, and Xiaomi.

In 2021, stocks that are more economically sensitive have soared as the pandemic recedes in some parts of the world. Many dividend payers have ridden this wave. The Morningstar Asia Dividend Yield Focus Index has been lifted by financial services constituents like Bank of China, Sun Hung Kai Properties, and United Overseas Bank. It has also benefited from dividend payers within the technology sector, including Taiwan Semiconductor and Infosys, as well as companies like Taiwan Cement, Denso, a Japanese consumer cyclical player, and Astella Pharmaceuticals.

What about income? The Morningstar Asia Dividend Yield Focus Index has a trailing 12-month yield of 3.8% as of May 31, 2021. That compares with just 1.8% for the Asia Large-Mid Cap Index.

Don’t Reach for Yield

There's nothing wrong with using dividend-paying stocks for income, but an investor's top priority must always be total return. Bad things happen when investors chase income too aggressively. High yield can equal high risk. Within the dividend-paying universe, the highest yields are often found in the most troubled areas. Lofty payouts often turn out to be unsustainable "dividend traps." For this reason, Morningstar dividend indexes screen companies for the sustainability of their payouts.

In 2020 and in years prior, companies with sustainable competitive advantages and strong financial health were likeliest to maintain their dividends. Among 2020’s dividend cutters in Asia, companies like PetrocChina, Nippon Steel, Geely Automobile, CK Hutchinson, PingAn Bank, Canon, and Ascendas were avoided because they were deemed by Morningstar Equity Research not to possess an economic moat around their business.

Meanwhile, some companies with economic moats failed the financial health screen, which relies on the Distance to Default metric. Incorporating both balance sheet information and market-driven inputs, the financial health requirement picks up on deteriorating that might foretell a dividend cut. Companies like Starhub, Komatsu, CK Asset Holdings, and Sinopharm are examples of companies that posses competitive advantages that position them to sustain profits and dividends long-term, but deteriorating financial health sent up red flags.

Dividends for the Long Term

The ups and downs of dividend paying stocks in 2020 and 2021 demonstrate that no investment strategy works all of the time. Thankfully, dividend investors tend to be more loyal than most, since they hold their assets not only for capital appreciation but also for total return.

Research shows that dividend payers are an excellent means of participating in equity markets. Not only do dividends allow investors to extract value from a portfolio without selling shares, but dividend growth and reinvested dividends also contribute a substantial portion of the long-term total return from stocks. Companies that can afford payouts to shareholders are more solid than most. Committing to a dividend can even instill discipline in corporate management.

But as 2020 shows, dividends are far from guaranteed, and a high yield is often a sign of trouble. For this reason, the Morningstar Asia Dividend Yield Focus Index screens for companies with economic moats and strong financial health. These attributes make equity income more sustainable.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)