Not an Easy Question…

Should retirees invest in stocks? The question cannot be answered with a yes or no. It is impossible to give a single answer valid for all retirees since it will depend on many factors. It will depend on the wealth situation of each individual, on the time horizon (it is not the same to invest when one is 65 years old than when one is 80 years old) and above all, on the level of risk that everyone can assume (in theory the level of risk decreases with age so that retired people, even if they have a constant flow of income via their public pension, should be more risk-averse than a 40-year-old investor).

But we must also take into account current market situations and the question must be understood as follows: assuming that the retiree can assume some risk, should he or she invest in stocks if he or she has a medium-long term horizon and wants to obtain some return on his savings? The answer is yes.

A long, long time ago, when interest rates were at 5 or 6% and bank deposits offered really attractive returns, retirees did not need to invest in stocks to get a decent return on their savings. It should also be said that when interest rates were high, inflation generally reached high levels as well.

Today, with interest rates at historically low levels or even in negative territory, it is very difficult to obtain a decent return by investing exclusively in fixed-income products.

In the investor’s mind there is also the idea that when one retires, it is time to consume ones’ savings and investments. The moment when ones retires is generally the line that marks the separation between the accumulation and the decumulation phases. In an ideal world (for those who have accumulated significant wealth) this may be true, but for the vast majority of retirees this image does not correspond to reality.

There are several reasons why many retirees will be forced to accumulate wealth during their retirement... at least those who could afford it.

The first reason is that our life expectancy is getting higher and higher. We are living longer and longer, therefore the retirement period is also getting longer (the retirement age was originally set at 65 because life expectancy was below that age). If we live longer, retirees need more money during their retirement period. That simple.

The second reason why retirees must continue to accumulate wealth is that if they do not do so, they will probably have difficulty in maintaining their standard of living. If they don't get a decent return for their money, they may even suffer the risk of consuming all the accumulated wealth.

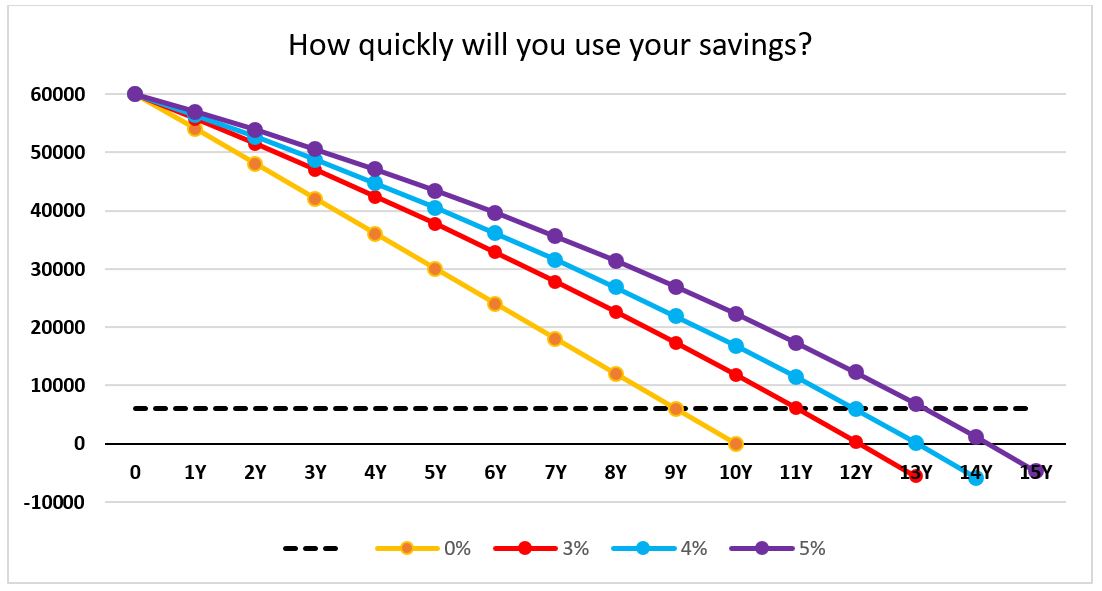

Let's assume the following example: A retiree has managed to save $60,000 which he intends to use to supplement his retirement. He will use $500 a month to complement his public pension. If he does nothing (i.e., he doesn't get any return on that capital) he will consume all his or her money after 10 years (the yellow line in the following graph). If he or she manages to get a return of 3% per year (red line) he or she will be able to supplement his or her pension for about 13 years (we have ignored the impact of inflation to simplify the calculations), 14 years if he/she gets a return of 4% per year and 15 years if he/she get a return of 5% per year.

The third reason is the possibility that public pensions will be increasingly reduced or at least the criteria for obtaining maximum pension levels will be tightened. We must bear in mind for example that one of the consequences of COVID-19 is that the governments have become even more indebted, increasing the pressure on public pensions. That means that retirees will have to count less on their public pension for the rest of their lives and they will have to count more on the money they can save and invest.

Not all Stocks

We see, therefore, that first saving and then getting an acceptable return on that money is going to be an essential issue for retirees. And considering the low interest rates that exist today, to get a good return there is no other way than investing in stocks. But that doesn't mean that if you're retired, you should invest all your money in stocks. Fixed income continues to play a crucial role in retirees' portfolios, perhaps not so much because of the returns it can offer but because of the protection it can provide in the event of a stock market fall.

Volatility Risk

One of the consequences of investing in stocks for a portfolio is that it will be more volatile. More than a risk, it is an intrinsic characteristic to investing in equities. Stocks fluctuate more than bonds. That's it. One has to take this into account and the only way to fight volatility is to increase the time horizon, but we should remind ourselves that not all retirees have the same time horizon.

Valuation Risk

As Christine Benz comments in this article (What High(ish) Equity Valuations Mean for Your Retirement Plan), “the prospect of a 10-year stretch of weak equity market returns shouldn't be a great concern for people who are many years from retirement. But what if you're getting close to retirement or are already retired? In that case, high equity valuations are more significant.”

“Lofty equity valuations make a good case for retirees starting out with a lower equity weighting. That's because sequencing risk is of most concern for new retirees,” adds Benz, “By starting out with more conservative portfolios, new retirees have a buffer of safe, nonequity assets that they can spend through as retirement progresses.”

“What I like is the optionality,” comments Benz, “If the stock market continues to perform well, the new retiree can subsist, at least in part, on the appreciation from the equity holdings. But if stocks slide, as high valuations suggest they could at some point, the retiree can use cash and bond holdings to meet living expenses.”

In theory, it makes a lot of sense for retirees to increase the weight of equities in their portfolios. But we should not forget the psychological impact. Increasing the weight of equities inevitably leads to increased volatility and can increase the risk of sequencing which can go beyond the the financial impact.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)