As incomes continue to rise in China, a bigger group of people have entered the cohort of potential luxury buyers, a tailwind that many global brands have not overlooked. However, luxury sales growth would seem to have met a speed bump under the Chinese government’s pledge to achieve “common prosperity”.

The common prosperity push encompasses efforts to ensure a fair distribution of wealth on the mainland. And the private sector is not far behind in embracing the theory – at least outwardly. In August, regulatory onslaught on various sectors including video games, education, and casinos collided with Chinese tech leader’s announcement of their intention to give away billions to support social initiatives. With a top-down agenda and a vow to reach social equity, Morningstar analysts expect consumers to rein in purchasing items with an air of extravagance.

The market finds similarities in this situation with the anti-bribery campaign back in 2012. Following that, demand for expensive goods moderated each year, with annual demand growth slowing from roughly 25% in 2012 to the pre-pandemic level of 10%.

Apart from that, Morningstar's senior equity analyst, Jelena Sokolova points to several more factors that could impede near-term luxury demand.

China’s zero-tolerance attitude to managing a local COVID outbreak may bring back district lockdown from time to time, especially in the period leading up to the Winter Olympics 2022. Additionally, tightening credit conditions and recent power shortages could play a part in dampening consumer sentiment. These will ultimately weigh on luxury consumption in the quarters to come.

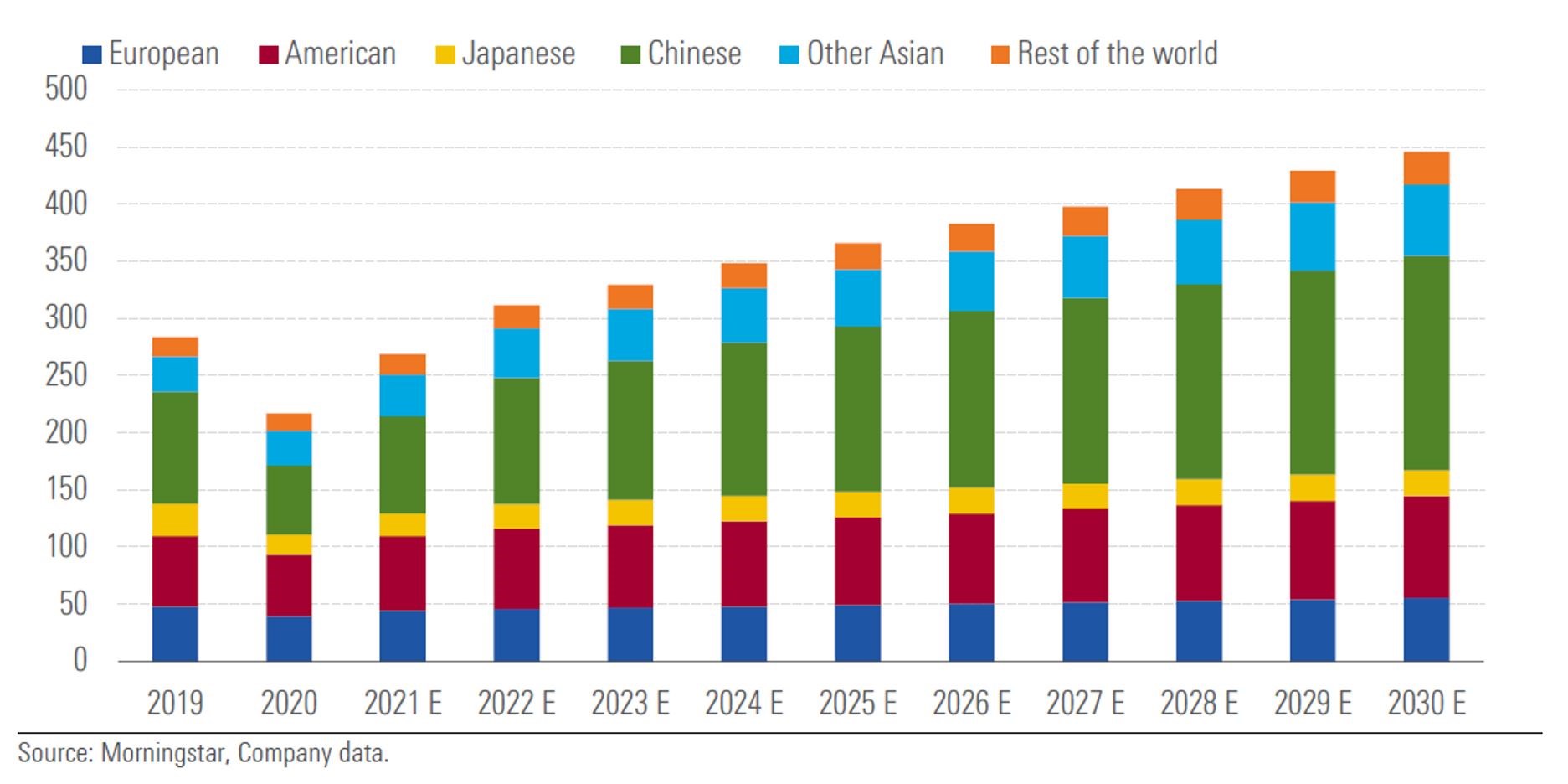

Looking at the anticipated numbers through 2030, though, Sokolova has confidence that the luxury demand growth coming from Chinese consumers will be a mainstay in the market, with its rate outpacing many of the major, developed markets. She continues: “These headwinds would probably be outweighed in the long run by the growing number of upper middle-class consumers; hence we retain our long-term forecasts for Chinese luxury consumption growth of around 6% annually to 2030 from 2019 levels.

Fig 1: China Demand Should Continue to Outgrow the Rest of World

The Shares Are Pricey, Too!

Under the common prosperity policy agenda, mainland spenders may fear judgement from others if seen to own or wear conspicuous luxury, and so are likely to steer away from logo-heavy items, which traditionally refer to products by Kering-owned Gucci or Louis Vuitton, a flagship brand under LVMH (MC).

Instead, according to Sokolova, brands with more discreet product offerings such as Hermes (RMS) or Bottega Veneta (owned by Kering KER) could be preferred.

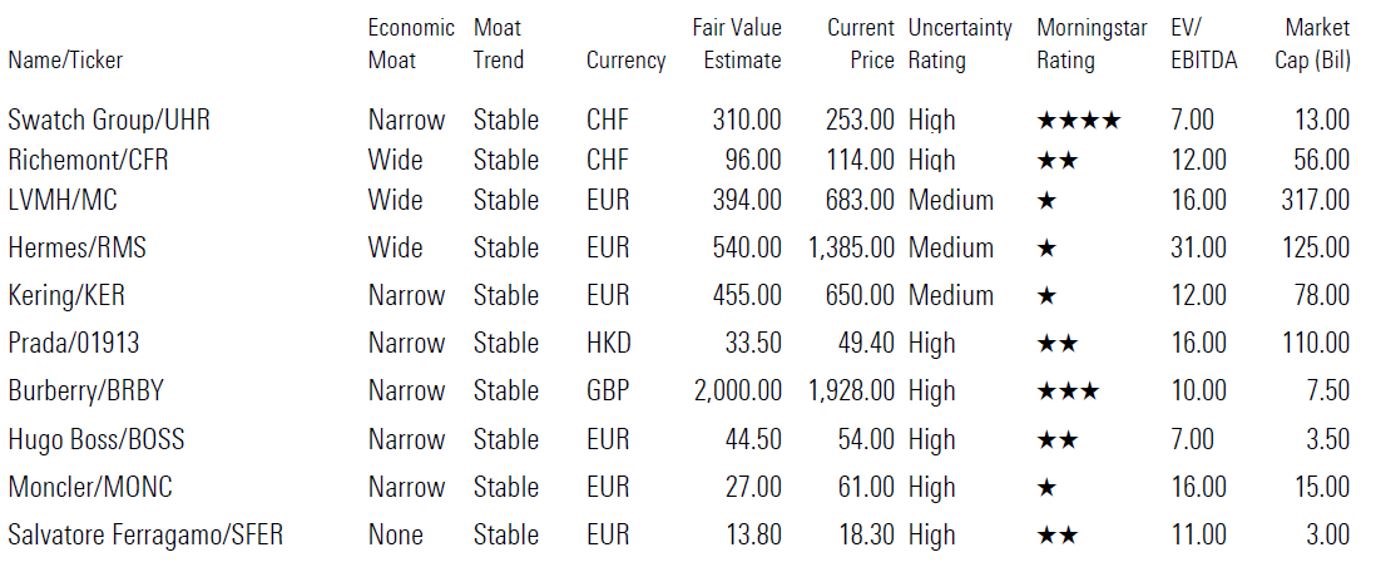

But Morningstar analysts see little justification for investors to buy into this trend in the stock market now. Almost all of these designer brands are expensive at present. Out of ten groups on our coverage, eight are viewed as overvalued. Shares in LVMH and Hermes are particularly pricey, indicated by their one-star Morningstar ratings.

“The luxury industry looks poised for a blue-sky scenario in 2021 amid strong sales rebound, leaving many luxury industry players trading near record levels. Nonetheless, we could not identify structural changes in the industry post-COVID-19 that would justify sustainably higher growth and profitability, and hence, valuations,” Sokolova says. For instance, Morningstar Direct data shows that Hermes’ stock trades a premium not only to its peers but also to its historic valuations.

Comparatively, Swatch Group (UHR) shares offer an attractive profile from both the earnings and the valuation perspective. The stock trades in the 4-star territory with more than 20% upside to Morningstar’s fair value estimate. While basic range brands continue to be challenged by smartwatches, the Swiss company has margin expansion opportunities elsewhere. In Sokolova’s view, some of the positive catalysts for the watchmaker seem overlooked by the market, including a positive brand mix effect and the automation and scaling of its Harry Winston jewelry brand. “We believe Swatch’s profitability should benefit from continued mix shift toward luxury and high-range watch brands, including Omega and Longines, which we believe to be the most profitable in the group,” explains Sokolova.

Fig 2 Most Luxury Brands under Morningstar Coverage Are Expensive

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")