Key Takeaways

- U.S. stock market trading at a discount to composite of our fair value estimates.

- However, expect a rough road ahead—tight monetary policy and decreasing credit availability will lead to economic slowdown.

- Deposit flight out of regional banks lowers their value, but this is not an omen of new financial crisis.

- Markets looking for a rebound in leading economic indicators to begin sustainable rally toward our fair value estimates.

Second-Quarter 2023 U.S. Stock Market Outlook

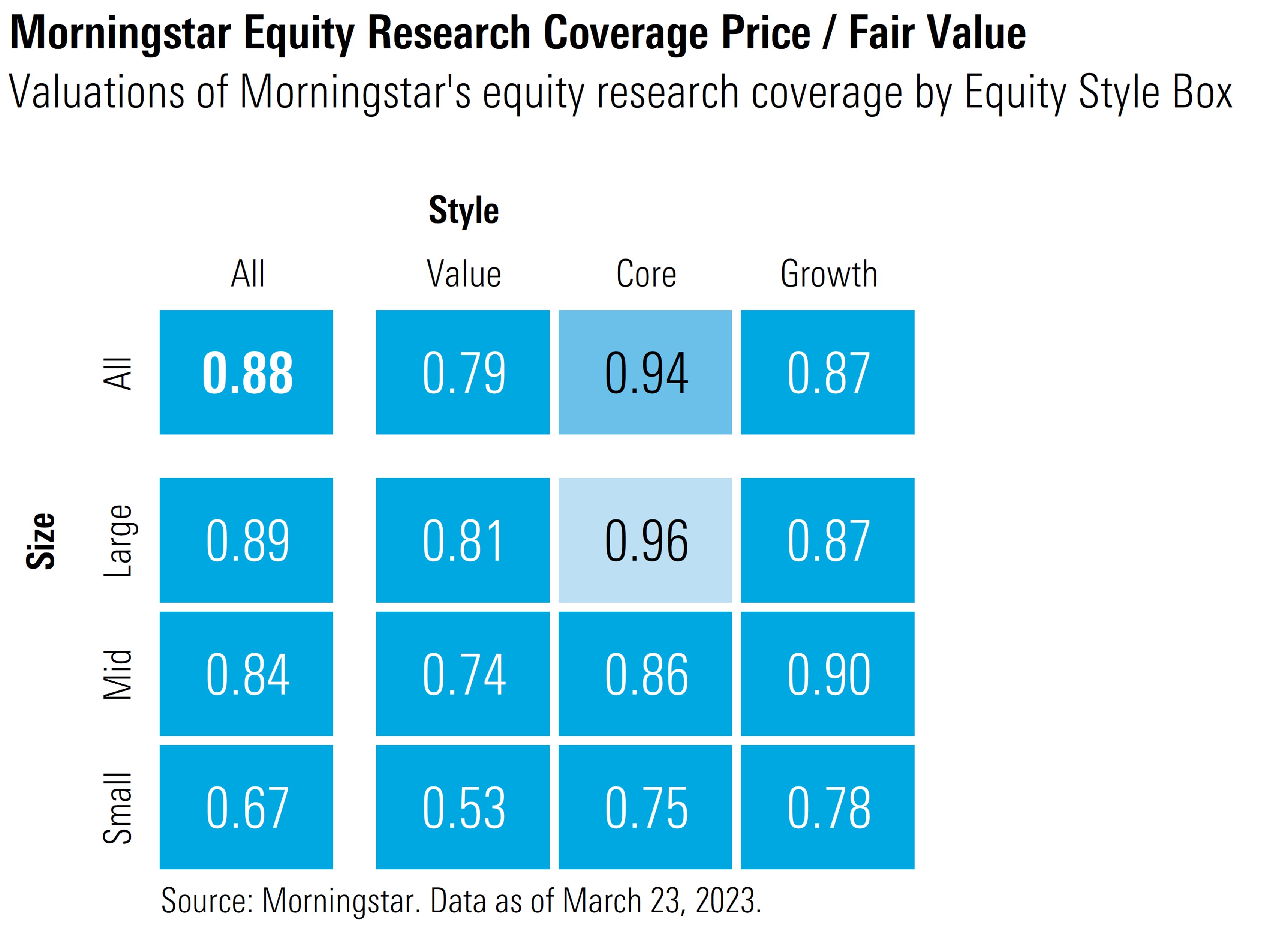

Stocks surged in January, coming off deeply undervalued levels and a technically oversold market in December. However, the market gave back almost half of those gains in February and March. According to a composite of the 700-plus stocks we cover that trade on U.S. exchanges, we calculate that as of March 23, the market was trading at a price/fair value of 0.88, a 12% discount to an aggregate of our intrinsic valuations.

According to our valuations, investors appear best positioned in a barbell-shaped portfolio by being overweight value and growth and underweight core. Both value and growth categories remain undervalued; albeit the growth category is much less undervalued than at the beginning of the year based on its outperformance for the year to date. The core category is much less attractive relative to the broader market average as it remains closer to fair value.

By capitalization, large-cap stock valuations have moved to a hair above the market average based on their outperformance in the first quarter. Mid-cap stock valuations are a little below the broad market average, whereas small-cap stock valuations remain exceptionally low, trading at a 33% discount.

While we calculate that the market is significantly undervalued, we also expect the markets are facing a rough road over the next few quarters. At this point, it appears the Fed is either at, or close to, the end of tightening monetary policy, inflation continues to abate, and long-term interest rates have topped out. However, we still think the economy will weaken in the second and third quarter.

While some of the headwinds we identified in our 2023 Stock Market Outlook have begun to dissipate, new headwinds such as deposit flight out of regional banks have begun to stir. The markets are close to the top of their trading range, and our near-term market forecast is that it will need to see a turnaround in leading economic indicators to break through the top of this range and rally upward to where we see fair value.

Stock Valuations Trading at a Deep Margin of Safety to Our Fair Value Estimates

Tightening monetary policy, a weak economy, high inflation, and rising interest rates took their toll on the markets in 2022, sending stocks deep into undervalued territory. Markets have begun to rebound but continue to trade at a wide margin of safety to our long-term intrinsic valuations. Since the end of 2010, the market has traded at or below the current discount only 10% of the time.

Deposit Flight and Bank Failures, an Opportunity or Omen?

In early March, Silicon Valley Bank announced that it was realizing losses in its hold-to-maturity book and would raise capital to cover the losses. Silicon Valley Bank was funded by an unusually high amount of uninsured deposits, and once these depositors became concerned about the safety of these deposits, it began an extraordinarily fast, modern-day bank run. Regulators swooped in and placed the bank in receivership once it became clear that the bank was no longer solvent.

Then began a widespread deposit flight out of small and regional banks, and soon thereafter, Signature Bank was also placed into receivership. Investors in regional bank stocks sold first and asked questions later, sending these stocks plummeting. Compounding the concern in the United States, Credit Suisse, one of the largest global banks, was also suffering its own issues and was forced into a bailout merger with UBS by Swiss regulators.

While we acknowledge there may be additional bank failures, we do not think this is the beginning of a new financial crisis. Except for the rapidity as to how fast these stock prices have fallen, the current situation is much different from what prompted the 2008 global financial crisis. While there are negative economic and market consequences to this liquidity crunch, it will not result in a wholesale freeze across the financial system. For greater detail on why this is not a precursor to another financial crisis, see Investment Impact of Banking Crisis.

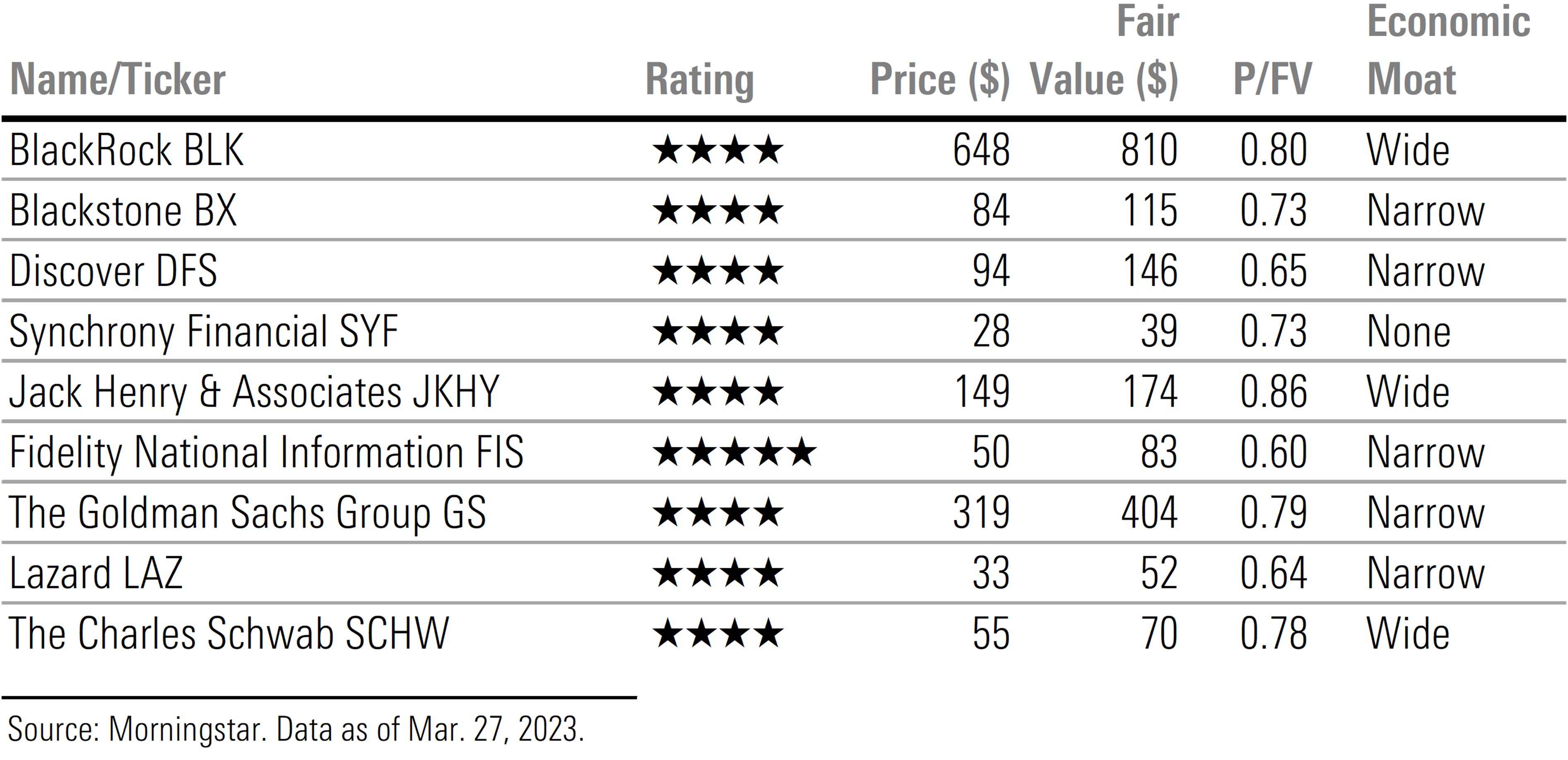

As regional bank stocks plummeted, contagion brought down the entire financial sector, even those nonbank financial companies that have either a very different business model from banks and/or have other funding options than deposits. Examples include investment banks/brokers, asset managers, credit card providers, and financial technology. We think this is an opportune time to look for stocks that have been unfairly dragged down with the carnage across the financial sector.

Headwinds to Turn Into Tailwinds in Late 2023

In our 2023 Market Outlook, we reviewed that this year would be a transition year from the headwinds we outlined in our 2022 Market Outlook into tailwinds we expect later this year:

- Slowing rate of economic growth to reaccelerate in fourth quarter.

- Monetary policy to pause, then pivot to easing.

- High inflation to moderate over course of the year.

- Rising long-term interest rates to roll over.

Here is what we see ahead:

Economic Outlook

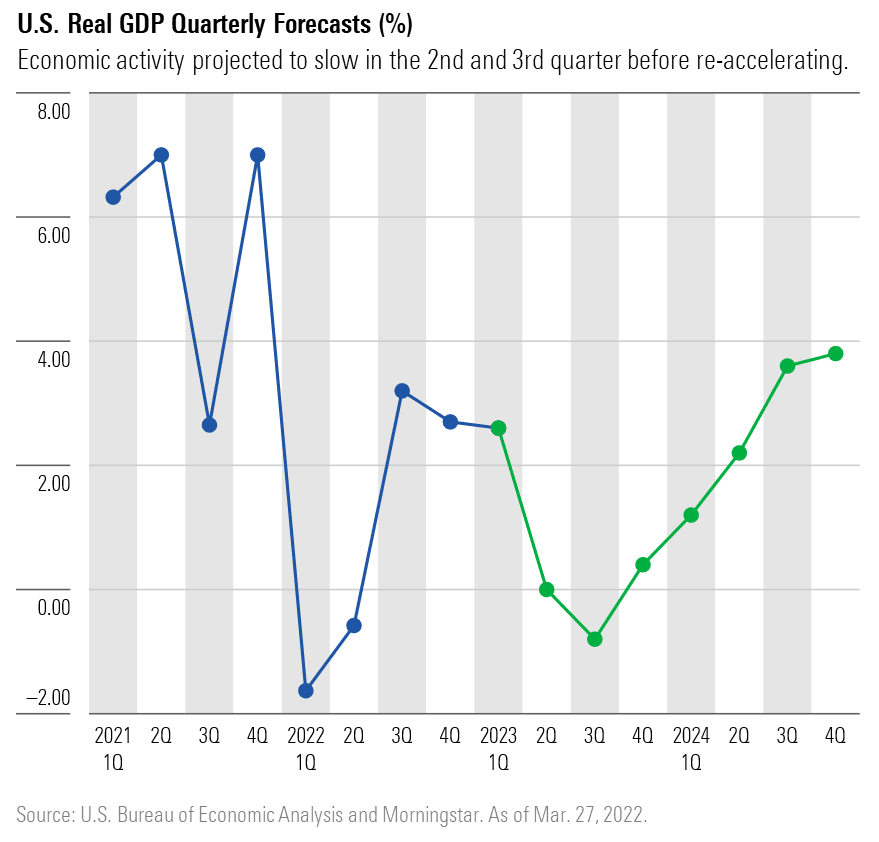

Even after accounting for the fact that monetary policy acts with a lag from when the Fed first begins to raise interest rates, the U.S. economy has been more resilient than we first projected. However, we project that tight monetary policy will take its toll and result in stagnant economic growth in the second and third quarters. We forecast real annualized U.S. gross domestic product of 2.6% in the first quarter will drop to 0% in the second quarter, contract by 0.8% in the third quarter, then reaccelerate to 0.4% in the fourth quarter. In our base case, our U.S. economics team does not foresee a recession, but should one occur, it expects it would be short and shallow. Looking forward, we forecast a 1.4% growth rate in 2024, but that economic momentum will build over the course of next year, leading to a 3.4% growth rate in 2025.

Monetary Policy

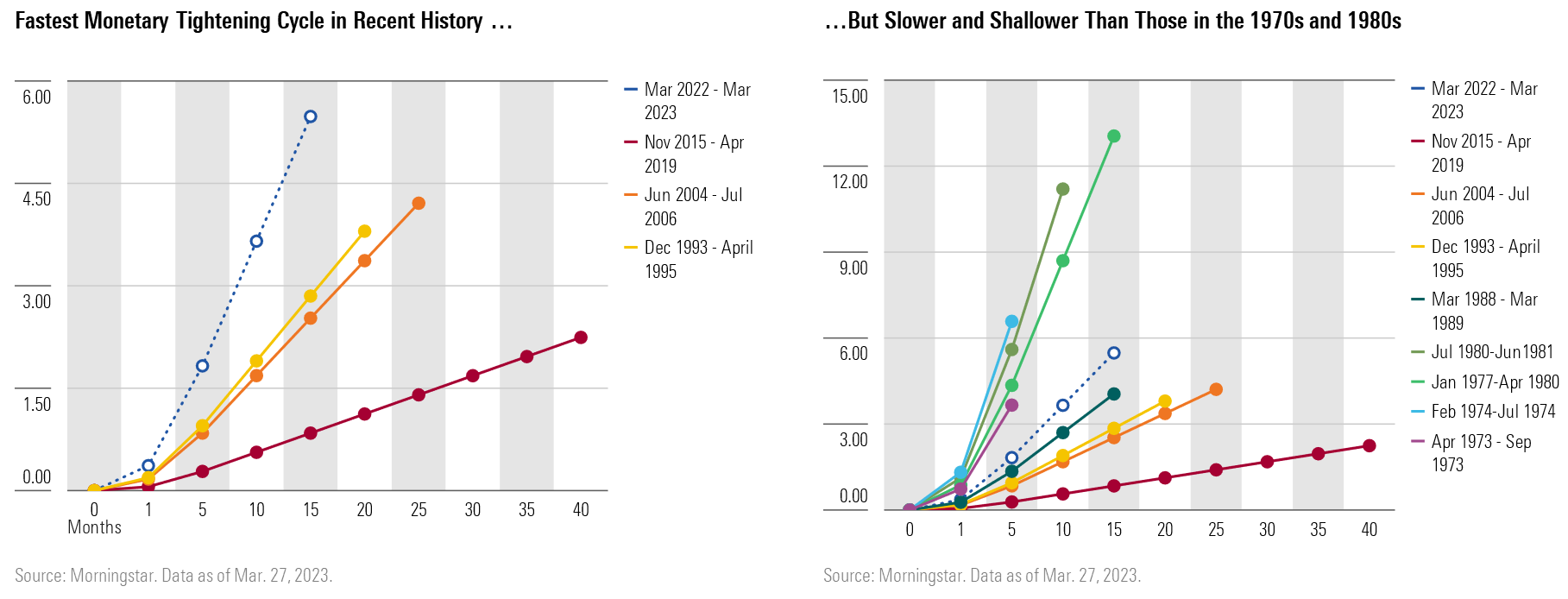

The Federal Reserve began tightening monetary policy in March 2022, one year ago. Since then, the federal-funds rate has risen from zero to a range of 4.75% to 5%, the fastest and steepest tightening policy since the early 1980s. Compounding the impact of hiking interest rates, the Fed had also begun a quantitative-tightening program that allows $95 billion of Treasuries and mortgage-backed securities to roll off its balance sheet each month.

At its March meeting, the Fed updated the language in its statement, removing “it anticipates ongoing increases” and replacing it with “anticipates that some additional monetary policy may be appropriate.” In addition, during the press conference, Chair Jerome Powell noted that the current issues among regional banks will result in tightening credit conditions that will have the same effect as one or more interest-rate hikes. At this point, it appears that we are either at, or near, the end of the current monetary tightening cycle.

Looking forward, we expect that a weak economy combined with waning inflation will provide the Federal Reserve with the room it will need to reverse course and begin to ease monetary policy at the end of this year.

Inflation Outlook

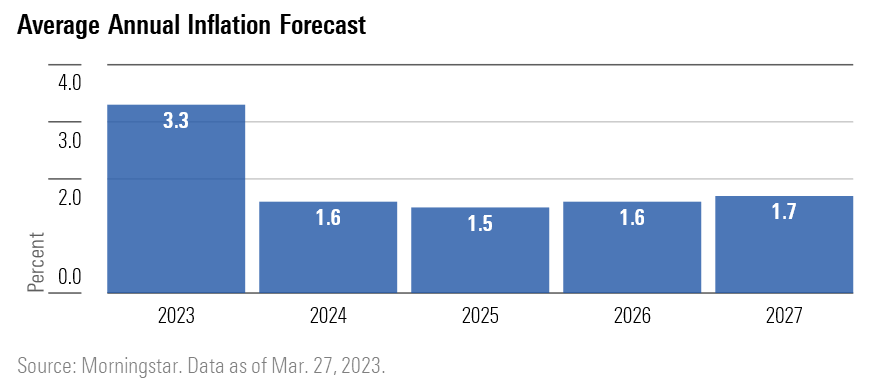

Inflation peaked last summer, and we forecast it will remain on a downward trend. While we project average annual inflation of 3.3% in 2023, we forecast that it will fall well below the Fed’s 2% target and remain below 2% for several years thereafter.

Interest-Rate Outlook

According to our forecasts, the preponderance of increases we expected in long-term interest rates in 2022 is behind us. The yields across the longer end of the curve may increase modestly in the near term as the Fed continues to sell bonds from its portfolio according to its quantitative-tightening program, but in the face of a stagnating economy, moderating inflation, and halt in further hikes to the federal-funds rate, we forecast interest rates will decrease slightly in the back half of the year.

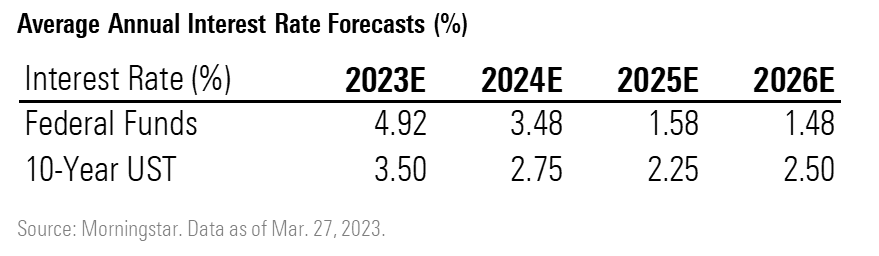

We forecast the yield on the 10-year U.S. Treasury will average 3.50% in 2023, decline to 2.75% in 2024, and bottom out at an average of 2.25% in 2025 before beginning to increase toward a normalized level. For greater detail, our 2023 fixed-income outlook is here.

.png)