Investors have been particularly wary of distribution out of capital, because it can result in an immediate decrease in the value of units. That means investors are left with a smaller amount of capital (as measured by NAV) after the distribution, than the amount they had started with, instead of earning more for the income.

However, there are serious consequences, more than just downsized capital. Reducing the fund size means that portfolio managers have less to maneuver in generating future returns. This is not ideal from a long-term investors’ perspective. Moreover, with the cash distribution, investors are to consider what to reinvest in and chances are missing out on some of the gains when sitting on cash and looking for reinvestments elsewhere.

A report authored by William Chow and Matias Möttöla at Morningstar finds that income funds may seem to pay more than the dividend offered naturally by the market. Most of them are unable to deliver a total return far above the income the funds paid out, which leads to an erosion of portfolio capital.

Most Challenged Asset Class

The report studied a sample universe of 185 funds for sale in Hong Kong. They are either 1. allocation or equity funds investing with an income-generating objective, or 2. fixed income funds. Each of the researched funds has at least US$100 million under management.

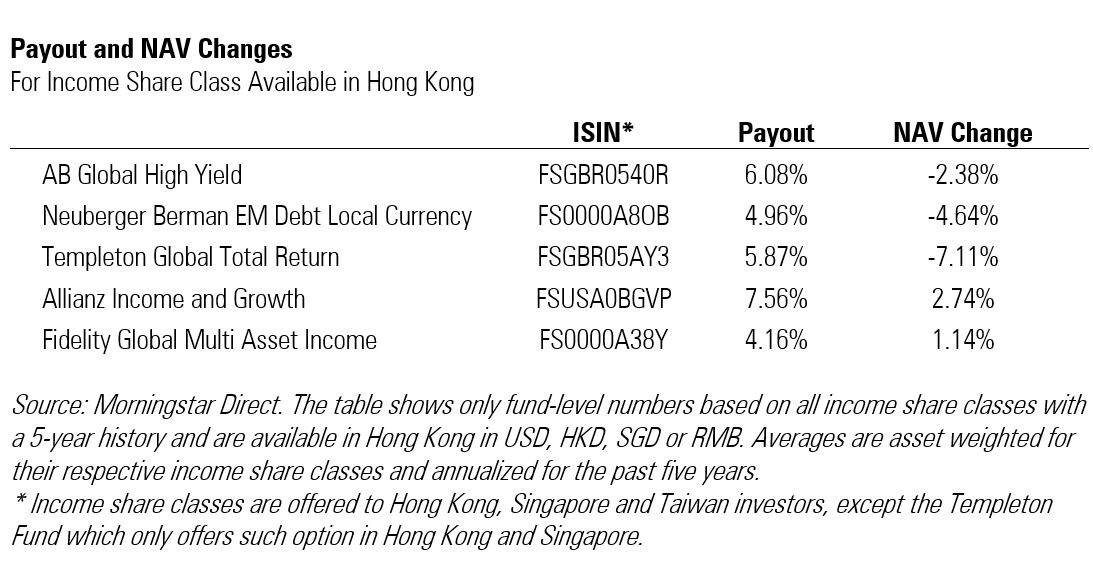

The report finds there is considerable variability between funds in each asset class, and fixed-income funds have had the largest challenges in shredding NAV from distribution.

Among the bond funds for sale in Hong Kong with a 4% or more annualized yield, three in four products ended up with a lower NAV than at the start of the period. Outside of the fixed income universe, analysts say the situation was relatively healthier. Allocation and equity funds that were unable to afford distributions without touching their capital amount to 13% and 25% of the sample universe, respectively.

Analysts explain that this is caused by a structural reason with bond funds. Fixed income securities have smaller upside potential than equities. Thus, these funds hardly sustain a high level of distribution for an extended period without the possibility of earning an impressive capital return. In order to match the promised dividend paid, managers take a great deal of risk. Within the fixed income world, this may mean going down the credit quality spectrum. On the one hand, these strategies can benefit from a strong market environment. On the other hand, their risk-return profile also could hurt in the long term. In a less sanguine market, from a total return perspective, fixed-income funds with high payouts will be heavily tested.

Avoid Higher Payout Frequency

Distribution frequency is another red flag. Funds that distributed more often tended to have higher aggregate payouts but are also prone to paying out from the capital.

On average, monthly distributing share classes made the highest payout yields, yielding above 4.2% per year for funds available for sale in Hong Kong, 4.5% in Singapore, and 4.4% in Taiwan.

The mechanism appeals to retirees for a simple reason. The income is distributed as if a person is on the job with day-to-day expenses being covered by the anticipated cash flow. Analysts remind investors that a steady level of income is not sustainable in funds that promise a monthly payout. Data show that each annual distribution of monthly share classes shrinks over time, as the funds reduced in size after high distributions. Lower-frequency distributions, like share classes offering an annual and semiannual distribution, would make lower payout yields that were generally not detrimental to capital.

Instead of exclusively chasing for high income payout, investors should factor in other attributes, such as fee and total return, before allocating capital to an investment product.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.

.png)

.jpg "Kate Lin")